The largest startup funding rounds in history are now measured in hundreds of billions, and four of the five biggest ever closed in a single quarter.

Our list tracks every mega-round that reshaped venture capital, who led it, what the capital is for, and what it signals about where the money is going next.

Largest Startup Funding Rounds: Key Findings

- The biggest mega-rounds now fund real assets like GPUs, factories, and fleets, not just growth projections.

- OpenAI, Anthropic, and SpaceX IPOs will test whether public markets support today’s trillion-dollar AI valuations.

- Companies like Stripe and Databricks prove late-stage investors still prioritize strong revenue before writing massive checks.

Q1 2026: One Quarter That Rewrote a Decade of History

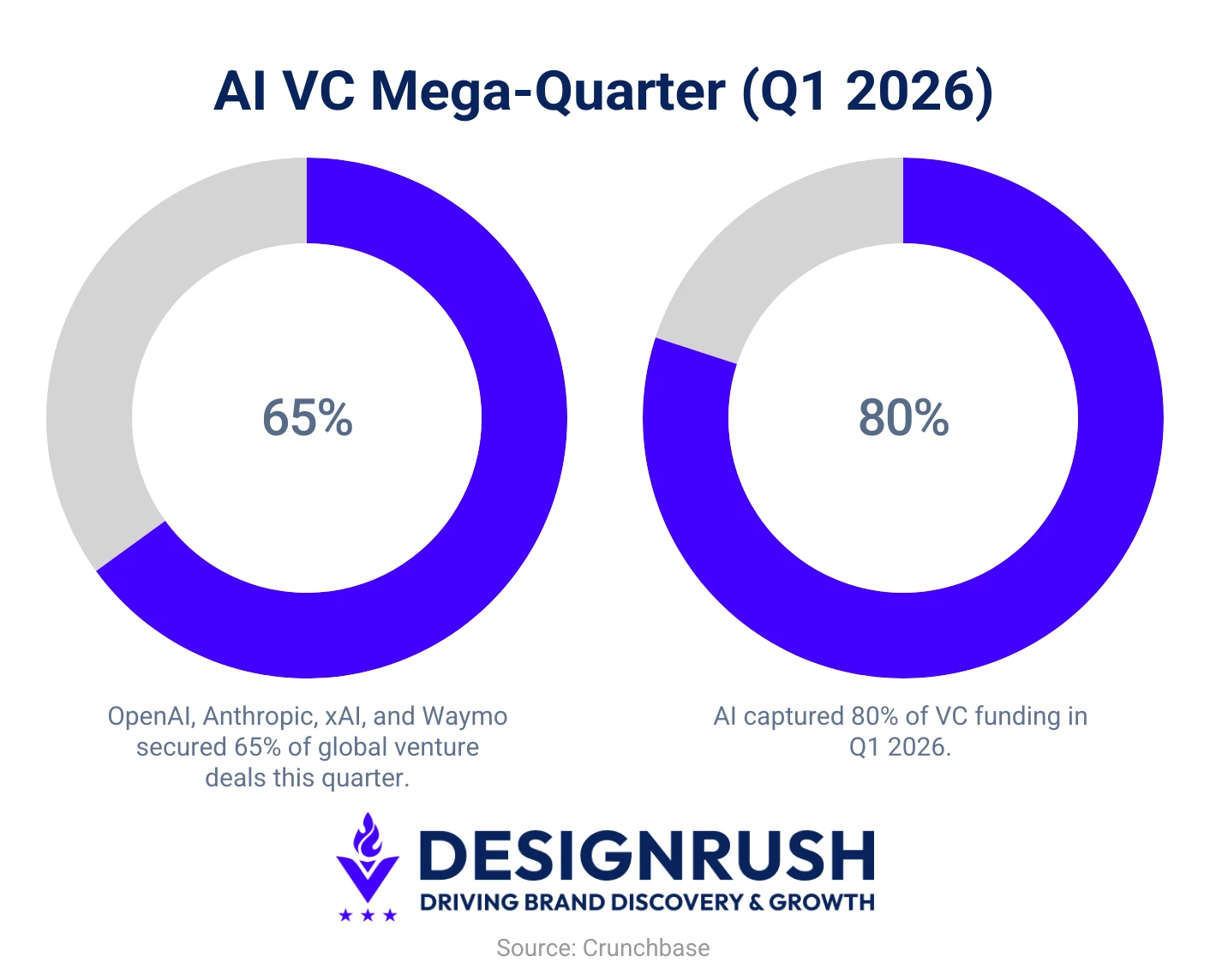

In just 90 days, OpenAI, Anthropic, xAI, and Waymo collectively raised $188 billion, roughly 65% of all global venture deals during the quarter.

AI overall captured about 80% of total VC funding in Q1 2026, with nine of the eleven companies on this list in AI or AI-adjacent sectors.

The model race is almost beside the point now. What matters is whether the rest of the venture market survives the concentration and whether public investors will pay what private ones already have.

The 20 Largest Startup Funding Single Rounds at a Glance

# | Company | Round Size | Year | Sector | Funding Stage |

1 | $122B | 2026 | AI/ML | Series F/private strategic financing | |

2 | $100B | 2017 | Multi-Sector Fund | Vision Fund/ sovereign capital raise | |

3 | $65B | 2026 | AI/ML | Series H | |

4 | $40B | 2025 | AI/ML | Late-stage funding round | |

5 | $30B | 2026 | AI/ML | Series G | |

6 | $20B | 2026 | AI/ML | Series E | |

7 | $16B | 2026 | Autonomous Vehicles | Series D | |

8 | $14.3B | 2025 | AI Infrastructure/ Data | Strategic investment (Meta) | |

9 | $13B | Sep 2025 | AI/ML | Series F | |

10 | $10B | Sep 2025 | AI/ML | Mixed debt/equity financing | |

11 | ~$10B | 2026 | Physical AI/ Industrial AI | Primary equity round | |

12 | $10B | 2024 | Data/AI | Series J | |

13 | $6.5B | 2023 | Fintech | Series I | |

14 | $6.2B | 2025 | AI Infrastructure | Seed (Founding Round) | |

15 | $5.6B | 2024 | Autonomous Vehicles | Series C | |

16 | $5.3B | Jul 2025 | AI/ML | Series B | |

17 | $5B | 2026 | Defense Technology/AI | Series H | |

18 | $4B | 2025 | Data/AI | Series L | |

19 | $3.5B | Mar 2025 | AI/ML | Funding round | |

20 | $2.5B | 2025 | Defense Technology/AI

| Series G |

Note on what follows: The detailed write-ups below cover the eleven companies represented across the 20 rounds, focusing on the single biggest funding event from each.

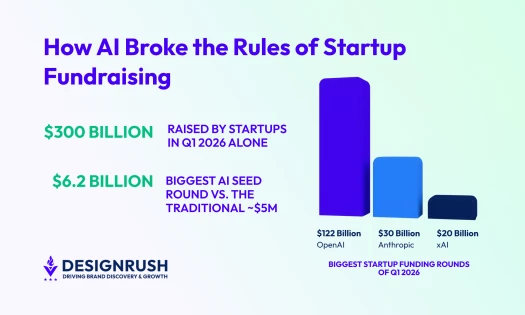

1. OpenAI - $122 Billion (2026)

- Funding stage: Private funding round/Series F - largest in Silicon Valley history

- Date: Closed March 2026 (opened at $110B in February 2026)

- Sector: AI/Machine Learning

- Round co-lead investors: SoftBank alongside Andreessen Horowitz, D.E. Shaw Ventures, MGX, TPG, and T. Rowe Price Associates; anchored by Amazon ($50B), NVIDIA ($30B), and SoftBank ($30B), with Microsoft also participating

- Post-money valuation: $852 billion

- What the capital is for: Next-generation compute infrastructure - custom silicon, $500 billion in AI data centers, and energy agreements under the Stargate program

OpenAI broke its own record: a $122 billion funding round only fourteen months after raising $40 billion, itself unprecedented at the time, yet it has already tripled.

No private company has ever reset the ceiling on fundraising so quickly, or so dramatically.

The round reportedly opened at $110 billion in February 2026, anchored by Softbank, Amazon, and NVIDIA. By close on March 31st, OpenAI had upsized it to $122 billion, pulling in more than $3 billion from individual investors through bank distribution channels.

OpenAI reportedly scaled from $1 billion in annual revenue to $2 billion in monthly revenue between 2024 and 2026, growing four times faster than Alphabet or Meta did at similar stages.

The IPO Could Come Very Soon

The funding round also set the stage for one of the biggest public-market debuts in history. OpenAI confidentially filed its S-1 on June 8, 2026, a week after Anthropic, with Goldman Sachs and Morgan Stanley as lead underwriters.

A September 2026 listing is the reported target, but OpenAI cautioned a listing "may be a while," and prediction markets put low odds on a debut before year-end. Hence, the timeline remains subject to SEC review and market conditions.

2. SoftBank Vision Fund - $100 Billion (2017)

- Round Type: LP-funded investment vehicle, not a single startup round

- Date: $93B first close May 2017; $100B total with later rounds

- Sector: Multi-Sector into mobility, real estate, eCommerce, and AI

- Lead LPs: Saudi Arabia Public Investment Fund ($45B), Abu Dhabi Mubadala ($15B), Apple, Foxconn, Sharp

- Key Portfolio: WeWork, Uber, Alibaba, Grab, ByteDance, DoorDash, Arm Holdings, and NVIDIA (early stake, sold prematurely)

The Vision Fund belongs on this list because it changed venture capital by permanently raising the ceiling for startup financing. Before 2017, even the largest venture funds managed around $3-5 billion.

SoftBank arrived with $100 billion and a mandate to fund dominant tech companies so aggressively that competitors could barely keep up. The strategy was to replicate Masayoshi Son’s Alibaba bet, arguably the most profitable single venture investment in history.

A Failed But Game-Changing Experiment

However, its biggest weakness was the pressure to deploy capital quickly. That led to inflated bets like WeWork, which reached a $47 billion valuation before collapsing. Softbank also exited NVIDIA too early, shares that later would have been worth over $150 billion.

By fiscal 2023, the Vision Fund posted a $32 billion annual loss, on top of $19 billion the prior year, taking cumulative losses past $50 billion.

Vision Fund 2, conceived as a $108B sequel, was ultimately self-funded by SoftBank with around $38 billion after most outside investors declined to participate.

Its legacy is complicated. The fund's losses were historic, but it also made today’s mega-rounds possible, including OpenAI's. It proved that capital markets were willing to back $100 billion tech ambitions, even as it struggled to prove the returns.

3. Anthropic - $65 Billion (2026)

- Funding stage: Series H

- Date: Closed May 28, 2026

- Sector: AI/Machine Learning

- Lead investors: Altimeter Capital, Dragoneer, Greenoaks, Sequoia Capital

- Post-money valuation: $965 billion, the highest valuation ever assigned to a private AI company

- What the capital is for: Safety and interpretability research, compute expansion to meet growing demand for Claude, and scaling the products and partnerships customers rely on

Anthropic's $65 billion Series H is the third-largest single private funding round in history, trailing only OpenAI's $122 billion round. At a $965 billion post-money valuation, Anthropic has officially surpassed OpenAI as the most valuable AI startup in the world.

The round is paired with a sweeping compute expansion. Anthropic has secured up to 5 gigawatts (GW) of capacity from Amazon, another 5 GW through Google and Broadcom, and additional GPU access through SpaceX's Colossus supercomputers.

Claude is now the first frontier model available on all three of the world's largest cloud platforms: Amazon Web Services, Google Cloud, and Microsoft Azure.

Its impact was dramatic enough to trigger a selloff across legacy SaaS stocks, fueling the so-called ‘SaaS apocalypse’, as investors began repricing around the threat of AI coding agents replacing parts of the traditional SaaS stack.

The Market Repriced Anthropic Overnight

The Series H closes out one of the most dramatic valuation runs on record. Anthropic's Series G in February 2026 valued the company at $380 billion.

By April, investors were offering terms at $800 billion. By May, the round closed at $965 billion, a near-tripling in value in under four months.

Anthropic confirmed a confidential S-1 on June 1, 2026, filing ahead of OpenAI, and is targeting a Q4 2026 debut, setting up one of the biggest AI rivalries ever to reach public markets within a single quarter.

4. xAI (Now SpaceXAI) - $20 Billion (2026)

- Funding stage: Series E (upsized from $15B target)

- Date: Closed January 2026

- Sector: AI/Machine Learning

- Lead investors: Valor Equity Partners, Stepstone Group, Fidelity Management & Research Company, Qatar Investment Authority, MGX, Baron Capital Group

- Post-money valuation: $230 billion at close, merged into SpaceXAI, valued at $1.25 trillion by February 2026

- What the capital is for: Accelerating compute infrastructure buildout, expanding Colossus supercomputer clusters, and developing consumer and enterprise AI products on Grok

In January 2026, the $20 billion Series E looked like another massive AI funding round, with investor demand exceeding xAI’s original $15 billion target.

Less than a month later, it became a footnote to something larger: the merger of SpaceX and xAI into a combined entity valued at $1.25 trillion, instantly the most valuable private company ever created.

NVIDIA, Cisco, and Tesla all participated financially, tying xAI’s compute expansion directly into Elon Musk’s broader ecosystem. xAI’s models were positioned as the intelligence layer for Tesla’s Optimus robots and autonomous vehicle fleet, while Grok reportedly reached 600 million monthly users across X.

SpaceX (which absorbed xAI in February 2026) went public on the Nasdaq on June 12, 2026, at a roughly $85.7 billion raise, the largest IPO in history, and closing its first day near a $2.1 trillion market value.

Why Even Rivals Needed Musk’s GPUs: The Anthropic Partnership

The Series E funded infrastructure. By late 2025, xAI’s Colossus facility in Memphis reportedly housed over one million H100 GPU equivalents, making it the world’s largest AI supercomputer cluster at the time.

The strangest twist came months later, when Anthropic, one of Musk’s fiercest AI rivals, signed a massive $45 billion compute deal with SpaceXAI to access Colossus capacity.

Your AI hates Whites & Asians, especially Chinese, heterosexuals and men.

— Elon Musk (@elonmusk) February 12, 2026

This is misanthropic and evil. Fix it.

Frankly, I don’t think there is anything you can do to escape the inevitable irony of Anthropic ending up being Misanthropic. You were doomed to this fate when you…

The deal reportedly included access to 220,000 NVIDIA GPUs at a moment when the demand for Claude Code was outpacing available supply.

The episode underscored a defining reality of the AI race: when one entity controls the world's largest GPU cluster, its rivals eventually come knocking, regardless of what anyone has said on X.

Same here.

— Elon Musk (@elonmusk) May 6, 2026

By way of background for those who care, I spent a lot of time last week with senior members of the Anthropic team to understand what they do to ensure Claude is good for humanity and was impressed.

Everyone I met was highly competent and cared a great deal about…

5. Waymo - $16 Billion (2026)

- Funding stage: Series D

- Date: February 2026

- Sector: Autonomous Vehicles/Applied AI

- Lead investors: Alphabet (majority), Dragoneer Investment Group, DST Global, Sequoia Capital

- Post-money valuation: $126 billion, more than doubling the $45 billion valuation from its October 2024 raise

- What the capital is for: Global city expansion, fleet scaling, and international launch, targeting 20+ additional markets in 2026, including Tokyo and London

Waymo's $16 billion round is the largest funding event in the history of autonomous vehicles.

It comes as Waymo finally crossed from a tech demo to real transportation infrastructure. In 2025, it served 15 million trips and surpassed 400,000 weekly rides across six U.S. cities.

Investors responded by valuing the company at $126 billion, nearly triple its $45 billion valuation just fifteen months earlier.

While OpenAI, Anthropic, and xAI are competing to own the intelligence layer of AI, Waymo is competing to own the physical deployment layer. Its moat is 127 million miles of driving data, a regulator-tested safety record, and a brand that riders trust with their lives.

The capital is now funding expansion city by city and vehicle by vehicle. Whether that bet holds will be determined in the next 24 months across 20 cities simultaneously.

6. Scale AI - $14.3 Billion (2025)

- Funding stage: Strategic investment by Meta (49% stake acquisition)

- Date: June 2025

- Sector: AI Data Infrastructure/Data Labeling

- Lead investors: Meta (sole investor)

- Post-money valuation: $29 billion

- What the capital is for: Acquiring founder Alexandr Wang and key AI talent while leaving Scale nominally independent

This entry requires clarification upfront: the $14.3 billion was not a conventional funding round. Meta did not invest to grow Scale AI. It invested to acquire Alexandr Wang in one of Silicon Valley’s largest AI acqui-hires.

Meta received a 49% non-voting stake, while most of the capital went to existing shareholders rather than Scale itself. The structure preserved the appearance of independence while limiting antitrust scrutiny.

The market reaction was immediate. OpenAI began winding down work with Scale, while Google and xAI paused contracts. Scale’s value depended on being the neutral infrastructure layer for competing AI labs, a position undermined by the fact that Meta owned nearly half the company.

The deal belongs on this list because of what it revealed about how expensive the AI talent war had become. Meta effectively paid billions for a founder and a small group of researchers because rebuilding equivalent expertise internally was seen as too slow and too risky.

7. Project Prometheus - ~$10 Billion (2026)

- Funding stage: Primary equity round (following $6.2B seed at launch in November 2025)

- Date: Finalizing at $10 billion as of April 2026; formal close not yet confirmed at time of publication

- Sector: Physical AI/Industrial AI

- Lead investors: BlackRock, JPMorgan, sovereign, and family-office investors

- Post-money valuation: $38 billion

- What the capital is for: Compute infrastructure, talent, proprietary industrial data, and R&D across aerospace, manufacturing, automotive, and drug discovery

The $10 billion round was unprecedented. Project Prometheus reached a $38 billion valuation just five months after launch, the fastest ascent to that scale in venture history.

Prometheus positioned itself around “physical AI”, applying frontier systems to factories, aerospace, manufacturing, and drug discovery rather than the digital economy alone.

Bezos’s $100B Industrial Acquisition Plan Behind Prometheus

The bigger story may be the $100 billion reportedly sitting alongside Prometheus. Jeff Bezos is said to be building a holding company to acquire industrial businesses whose proprietary operating data could train Prometheus models directly.

The logic mirrors Berkshire Hathaway’s industrial portfolio: own the business, harvest the data, train the model, redeploy the model into the business.

It’s an attempt to solve the hardest problem in physical AI: access to proprietary real-world training data locked inside factories, sensor systems, and engineering workflows that competitors cannot access.

Bezos described AI in 2025 as an “industrial bubble,” arguing that the companies building real-world industrial capability would be the ones left standing when it bursts.

8. Databricks - $10 Billion Equity/$15.3 Billion Total (2024-2025)

- Funding stage: Series J

- Date: Announced December 2024; closed January 2025

- Sector: Data Infrastructure/AI

- Lead investors: Thrive Capital, Andreessen Horowitz, DST Global, GIC, Insight Partners, Meta, and others

- Post-money valuation: $62 billion

- What the capital is for: AI product development, acquisitions, expansion, and employee liquidity

OpenAI, Anthropic, and xAI are competing to build the most capable intelligence layer; Databricks is competing to own the data layer that makes that intelligence usable at enterprise scale.

By the time the Series J closed, Databricks had crossed a $3 billion revenue run rate, posted 60%+ year-over-year growth for multiple quarters, and generated positive free cash flow for the first time in company history.

More than 10,000 organizations, including over 60% of the Fortune 500, relied on Databricks at the time of the raise.

Alongside the $10 billion equity raise – the largest venture deal of 2024 – Databricks secured a $5.25 billion debt facility from major Wall Street banks, which signals the maturity to access cheaper capital while preserving IPO flexibility.

The long-anticipated IPO remains the next chapter for 2026, with Databricks currently valued at $134 billion following its $5 billion Series L round last December 2025.

9. Stripe - $6.5 Billion (2023)

- Funding stage: Series I (explicitly non-dilutive)

- Date: March 2023

- Sector: Financial Infrastructure/Payments

- Lead investors: Andreessen Horowitz, Founders Fund, Thrive Capital, Goldman Sachs Asset and Wealth Management, GIC, Temasek, General Catalyst, Baillie Gifford, MSD Partners

- Post-money valuation: $50 billion; back to $159 billion via February 2026 tender offer

- What the capital is for: Employee liquidity and tax obligations tied to equity awards

Stripe’s Series I was less a funding round than a financial management event. The company said it did not need the capital to operate; the $6.5 billion was raised primarily to help employees sell shares and cover tax obligations after more than a decade as a private company.

The round also became one of the clearest valuation resets for the post-2021 tech correction. Stripe accepted a $50 billion valuation, down 47% from its peak, while many late-stage startups avoided rising altogether.

What followed mattered more. Stripe reached profitability in 2024 without raising more equity, while secondary share sales reportedly pushed its valuation back above $159 billion by 2026.

At the same time, acquisitions like Bridge, Privy, and Metronome repositioned Stripe beyond payments and into the financial infrastructure layer of the AI economy.

10. Anduril Industries - $5 Billion (2026)

- Funding stage: Series H

- Date: May 2026

- Sector: Defense Technology/Autonomous Weapons/AI

- Lead investors: Thrive Capital and Andreessen Horowitz

- Post-money valuation: $61 billion

- What the capital is for: Arsenal-1 manufacturing buildout, autonomous weapons production, and expansion of the Lattice software platform

Anduril’s Series H capped one of the fastest valuation climbs in defense-tech history, rising from $14 billion in 2024 to $61 billion less than two years later.

The company generated $2.2 billion in 2025 revenue while securing major defense contracts, including a 10-year U.S. Army deal with a $20 billion ceiling and a role in Trump’s $185 billion Golden Dome missile defense initiative.

The round reflected a broader shift in defense investing: while traditional contractors rely on slow procurement cycles, Anduril Industries built around software-defined warfare and autonomous systems measured in months rather than decades.

AI’s Shift From Software to Weapons Production

The centerpiece was Arsenal-1, a high-rate production facility paired with ArsenalOS, the software platform managing manufacturing throughput.

The same day Series H closed, the Department of Defense announced an agreement for Anduril to supply more than 10,000 low-cost hypersonic missiles over three years.

Largest Startups by Total Cumulative Funding - Beyond the Single Round

A company that raises $5 billion across seven rounds over ten years is telling a different story than one that raises $14 billion in a single peak-market moment.

The cumulative table shows which companies have sustained investor confidence across multiple market cycles, which is a much harder signal to fake than a single large round.

# | Company | Est. Total Raised | Largest Single Round | # of Rounds | What That Means in Practice |

1 | OpenAI | ~$165B+ | $122B (2026) | 7+ | No private company in history comes close on a cumulative basis. |

2 | Anthropic | ~$137B+ | $65B Series H (2026) | 18+ | Now the fastest cumulative ramp from zero to $100B+ in venture history. |

3 | SpaceX + xAI | ~$50B+ combined | $20B Series E, xAI (2026) | 10+ | Post-merger. Definitive figures will appear in the IPO prospectus. |

4 | Uber | ~$24B+ | $13.2B (2018) | 10+ | Raised across a decade from SoftBank, Benchmark, Google, and others. Now profitable as a public company, justifying the aggregate capital. |

5 | WeWork | ~$22B+ | $12.8B (2019) | 10+ | The worst capital outcome on the list. Most of this became worthless when Chapter 11 filed in 2023. |

6 | Databricks | ~$16B+ | $10B (2024-25) | 8+ | Each round came at a higher valuation than the last, reflecting real ARR growth. Rare on this list. |

7 | Scale AI | ~$15B+ | $14.3B (2025) | 5+ | Most of the total came in a single raise. Earlier rounds were modest. The $14.3B reflects the market's sudden recognition that labeled data is the scarce resource. |

8 | Waymo | ~$11B+ | $5.6B Series C (2024) | 4+ | Alphabet's balance sheet funded years of R&D before external capital entered. |

9 | Anduril | ~$11.3B | $5B Series H (2026) | 8 | Rose from $127M seed in 2019 to $61B valuation in seven years; the fastest climb in defense-tech history. |

10 | Stripe | ~$9B+ | $6.5B Series I (2023) | 6+ | The least capital per dollar of enterprise value on this list. Profitable before its largest round. |

The gap between OpenAI and everyone else is staggering. ~$165 billion in total external funding is more than the GDP of most countries.

It reflects both the belief that AGI could become a multi-trillion-dollar market and the reality that training frontier AI models now requires infrastructure spending previously reserved for building national utilities.

How Mega-Rounds Have Grown: A Timeline of Record-Breaking Funding

Startup mega-rounds have always come in waves. Each one triggered by a new thesis, a new class of investors, or a technology that needed infrastructure-scale capital to exist at all:

- Phase 1 (2017-2020) SoftBank's 2017 Vision Fund was the first real step-change: sovereign-wealth-backed, growth-stage pools that dwarfed traditional venture funds and forced entire sectors to reprice.

- Phase 2 (2021-2022) bull market peak piled on, where mobility, super-apps, and Asian ecommerce raised $10B+ on optimistic multiples.

- Phase 3 (2023-2024) saw funding cool, but SpaceX and Stripe quietly proved that capital-efficient companies could still command extraordinary valuations.

- Phase 4 (2025) pushed AI funding into a different league, led by OpenAI’s $40B raise and multi-billion-dollar rounds for Anthropic and xAI. The boom was fueled by sovereign wealth money like Saudi Arabia’s PIF and massive AI infrastructure costs.

Then Q1 2026 made 2025 look like a warmup. Investors poured $297 billion into startups globally in the quarter, an all-time record, up over 150% year over year.

Year-by-Year: Largest Funding Round by Year (2017-2026)

Year | Company | Round Size | Notable Context |

2017 | SoftBank Vision Fund | $100B | First fund to deploy at this scale; sovereign wealth entered venture for the first time at this size. |

2019 | WeWork | $12.8B | Largest private real estate / co-working raise; valuation collapsed from $47B to near-zero within months. |

2023 | SpaceX | ~$12B | Infrastructure-scale defense and launch tech; validated reusable rocket economics and Starlink broadband thesis simultaneously. |

2024 | Databricks | $10B | Largest data/AI platform round at the time; foreshadowed 2025-2026 AI surge. |

2025 | Anthropic | $13B | Safety-focused AI rival to OpenAI closed a Series F backed by Google and Amazon |

2025 | Scale AI | $14.3B | Largest AI data-labeling raise ever; Amazon and Meta confirmed that clean training data is as valuable as the model itself. |

2025 | OpenAI | $40B | Shattered all prior startup round records; SoftBank and Thrive Capital led at a $300B post-money valuation. |

2026 (Q1) | OpenAI | $122B | New all-time record, reshuffling the entire list; Q1 2026 global funding hit $297B - 2.5× the prior record. |

2026 (Q2) | Anthropic | $65B | Third-largest round in history; $965B valuation makes Anthropic the most valuable private AI company in the world. |

Which Sectors Are Attracting the Largest Funding Rounds?

18 of the top 20 rounds on our list are AI or AI-adjacent, from foundation models like OpenAI to infrastructure like Scale AI.

It reflects an increasingly global capital shift toward a single belief: that AI will define the next economic cycle.

Outside AI, the funding landscape is still revealing:

- Healthcare and biotech attracted roughly $71.7 billion globally in 2025, even without producing a top-20 mega-round.

- Financial services captured $52 billion (up from $41 billion in 2024), led by Stripe and a new generation of embedded-finance platforms.

- Defense technology and autonomous systems are the fastest-emerging mega-round sectors, led by Anduril Industries and Waymo.

Largest Funding Round by Sector

Sector | Top Company | Round Size | Year | Insight/Trend |

AI / ML (Foundation Models) | OpenAI | $122B | 2026 | Driven by AGI expectations and compute demand |

Autonomous Vehicles | Waymo | $16B | 2026 | Autonomous driving is now a long-term infrastructure bet. |

AI / Data & Infrastructure | Scale AI | $14.3B | 2025 | Training data recognized as a strategic asset |

Coworking / Real Estate | WeWork | $12.8B | 2019 | Cautionary tale of narrative-driven overfunding; Chapter 11 bankruptcy in 2023. |

Fintech | Stripe | $6.5B | 2023 | Investors shifted toward profitable fintech platforms. |

Defense Tech | Anduril | $5B | 2025 | First VC-backed defense prime; accelerated by the Russia-Ukraine conflict. |

Five Firms, Trillions in Capital: The Investors Behind Every Mega-Round

The top 20 is dominated by five recurring firms. At this scale, the lead investor's reputation draws the rest of the group in. Meaning, who writes the largest checks signals which sectors are driving the next wave of capital.

1. Andreessen Horowitz (a16z): Backing the Infrastructure Beneath AI

- Fund size: ~$90 billion+ AUM

- Mega-rounds on list: 6

- Investment thesis: AI infrastructure as the new TCP/IP

- Notable outcomes: SpaceX, Databricks, Stripe, and Anduril

a16z is one of the defining investors of the current AI and infrastructure cycle. The firm is a lead or major co-investor in at least five companies on this list: SpaceXAI, Databricks, Stripe, Anduril Industries, and Anthropic.

The firm backs companies positioned to become infrastructure for entire sectors, including rocket launch infrastructure, AI data infrastructure, defense infrastructure, and increasingly, AI itself.

2. Thrive Capital: The Investor Behind OpenAI’s Funding Rounds

- Fund size:$50 billion+ AUM

- Mega-rounds on list: 4

- Investment thesis: Long-horizon consumer and AI bets; concentrated positions

- Notable outcomes: OpenAI (lead on $40B and $122B rounds)

Thrive Capital may be the most influential investor on this list in terms of capital leverage. It led OpenAI’s $40B validating valuations large enough to bring in investors like SoftBank Group, which enabled the rounds to close at the sizes they did.

Thrive’s thesis is taking long-term positions in category-defining AI and consumer companies, even at valuations that initially seem aggressive.

They’re also an early Anysphere investor, which reflects the same pattern: identify the likely market leader early, lead a round at an uncomfortable valuation, and hold.

3. SoftBank: Betting Billions on Category Dominance

- Fund size: ~$100 billion (Fund 1)

- Mega-rounds on list: 3

- Investment thesis: Dominant global market leaders; network-effect defensibility

- Notable outcomes: Alibaba (massive win); WeWork (complete loss)

SoftBank’s participation in both the WeWork disaster and OpenAI’s two record rounds reveals a consistent investment thesis: back the company most likely to dominate a global category.

The difference is that OpenAI has the revenue growth and market position to support that narrative, while WeWork ultimately did not.

SoftBank is a high-conviction momentum investor, and momentum investors produce enormous wins when the narrative holds, but equally large losses when it breaks.

4. Google and Amazon: Cloud Giants Investing to Lock In AI

- Mega-rounds on list: 3

- Investment thesis: Strategic AI and infrastructure investments

- Notable outcomes: Anthropic, Waymo, DeepMind

Google and Amazon are not traditional venture investors, but they are strategic investors using AI partnerships to strengthen their cloud platforms.

Google backed Anthropic to ensure Claude runs on Google Cloud, while Amazon backed Anthropic and Scale AI to ensure enterprise AI workloads run through AWS.

That changes the economics of these deals. Even without an IPO, Google and Amazon still benefit from the long-term cloud revenue and commercial relationships. This makes them more willing than pure financial investors to support mega-round valuations.

5. Founders Fund: The Contrarian Firm That Bets on Hard Tech

- Fund size: $17 billion+ AUM

- Mega-rounds on list: 4

- Investment thesis: Contrarian science and deep-tech bets; anti-consensus

- Notable outcomes: SpaceX, Anduril, Stripe

Founders Fund is a Silicon Valley venture firm known for backing high-risk, unconventional technology bets.

The firm backs both SpaceXAI and Anduril Industries, which are companies building hard physical technology and defense systems when the rest of the market is chasing software.

That strategy made Founders Fund one of the few contrarian firms in venture capital. Its early investment in SpaceX became one of the most successful VC bets ever as the company’s valuation later surpassed $1 trillion.

What It Takes to Raise a Mega-Round - Lessons from the Top 20

These observations come directly from what separated the companies that worked from the ones that didn’t. Across 20 rounds, the patterns look more like principles than coincidences:

- The lead investor’s yes usually defines the round

- Not needing the money is the strongest negotiating position

- Governance concessions cost less than founders think

- The strongest mega-rounds are tied to real infrastructure

- Most mega-rounds still require revenue first

- The biggest rounds happen after institutions decide the category matters

1. The Lead Investor’s Yes Usually Defines the Round

Thrive Capital, leading the round at $300 billion, absorbed the credibility risk that made SoftBank’s $30 billion participation, which came in as the largest single check, possible.

Google leading Anthropic’s early rounds made Amazon’s participation almost inevitable, because once one hyperscaler has made an AI bet at scale, its cloud rival cannot afford not to.

Mega-round syndicates form around one decision, and everything else is a response to that decision. Your job is to get the one yes, then let it pull the round together.

2. Not Needing the Money Is the Strongest Negotiating Position

Stripe’s $6.5 billion Series I was explicitly non-dilutive, raised mainly for employee liquidity and tax obligations tied to older equity awards. Because the company was already profitable, it could dictate the terms rather than accept them.

It deliberately repriced to a $50 billion valuation, prioritizing a cleaner IPO path over defending inflated optics. By 2026, secondary sales had already pushed Stripe’s implied valuation back above $159 billion. Companies forced to raise defensively rarely get that kind of outcome.

3. Governance Concessions Cost Less than Founders Think

WeWork’s collapse traces directly to a governance structure that made it difficult to stop capital from compounding a broken business model. Adam Neumann’s unchecked voting control meant no board could force a correction before the company ran out of road.

The opposite happened at Uber, where SoftBank’s investment created the leverage needed for the leadership changes that later enabled profitability.

Independent board members with real authority are insurance against capital being wasted on a thesis that stopped working.

4. The Strongest Mega-Rounds Are Tied to Real Infrastructure

OpenAI’s $40B and $122B rounds were tied to concrete Stargate infrastructure commitments: data centers, GPU contracts, and energy agreements.

Anduril Industries linked its $5 billion Series H to Arsenal-1 manufacturing capacity, while the Department of Defense simultaneously announced a major missile contract.

That’s the ideal version of a mega-round: infrastructure expansion and customer demand becoming visible at the same time. Investors trust build schedules and physical assets more than revenue forecasts alone.

5. Most Mega-Rounds Still Require Revenue First

Most companies on this list reached a major revenue scale before raising their biggest rounds. Databricks, Anthropic, and Cursor all had massive revenue before their largest raises.

The exceptions followed a different logic entirely. Scale AI was effectively an acqui-hire by Meta, while Project Prometheus raised billions before launch because investors were backing the team and thesis, not traction.

Revenue first is still the rule. Team-and-thesis bets are the exception.

6. The Biggest Rounds Happen After Institutions Decide the Category Matters

The biggest structural shift in mega-rounds over the last decade is the rise of sovereign wealth funds as permanent AI investors.

Saudi Arabia’s PIF anchored SoftBank’s Vision Fund with $45 billion, while Mubadala, QIA, and MGX appeared across multiple rounds on this list.

These funds already have AI allocation mandates, meaning they are no longer asking whether to invest in the category, only where. Founders positioned at the center of those mandates are no longer facing skepticism and are seeing demand rise.

Future Trends & Where AI Is Heading: Is the AI Funding Bubble Going to Burst?

This is the question behind the entire list. Two of the most credible voices in finance disagree sharply, and the answer may depend less on AI itself than on the financial structure forming around it.

Here’s the honest read on the future trends of AI:

- The bear case - Concentration risk and the cascade scenario

- The bull case counterpoint - Real infrastructure, real revenue, and a historical precedent

- The IPO convergence: What happens when four trillion-dollar companies go public

1. The Bear Case - Concentration Risk and the Cascade Scenario

Michael Burry, the contrarian investor who famously shorted the 2008 housing market, is sounding the alarm again, this time on AI concentration risk.

Per Slok, 87% of VC funding is directed at AI, 49% of investment grade bond issuance is AI, and 38% of high yield bond issuance is linked to AI.

— Cassandra Unchained (@michaeljburry) May 19, 2026

During the internet boom, in 1999, less than 40% of VC funding was linked to internet companies.

Broadening to the wider… pic.twitter.com/Ibo3eRPVYA

The skeptical argument is not that AI is bad technology. It’s that the financial structure forming around it increasingly resembles the setup preceding the dot-com crash.

AI Capital Is Concentrating at Historic Levels

AI firms captured 61% of global venture capital in 2025, $258.7 billion out of $427.1 billion total, more than double AI’s share in 2022, according to OECD analysis.

The concentration has only sharpened in 2026. In Q1 alone, AI accounted for roughly 80% of total VC funding, with just four companies, OpenAI, Anthropic, xAI, and Waymo, raising $188 billion, or about 65% of all global venture investment for the quarter (Crunchbase News).

The dot-com parallel is uncomfortable:

At the peak of that era, TMT (technology, media, and telecom) companies accounted for more than 90% of venture capital investment, backed largely by firms yet to generate profits.

When sentiment broke in 2000, the NASDAQ declined 78% over the next two years, wiping out over $5 trillion in market value. IPO volume collapsed from 476 listings in 1999 to just 80 in 2001, a near-total shutdown that took years to reopen.

Why Concentration Creates Cascade Risk

According to Apollo Global Management research, roughly 87% of venture capital flows are now tied to AI. If sentiment weakens, much of the venture market slows with it because so much capital is concentrated in the same category.

The concentration is even narrower at the top:

- 73% of total AI investment value is now in mega-rounds above $100M, meaning a sentiment shift hits the majority of deployed capital all at once.

- ~50% of all AI funding sits in rounds above $1 billion, a level of concentration with almost no modern precedent outside the dot-com peak.

That works while confidence holds. But if growth slows or public markets reject the valuations, late-stage rounds disappear, and companies dependent on continuous capital suddenly run out of options.

The Debt Layer Is Where the Risk Becomes Systemic

The deeper concern is how much money is being committed before the long-term economics are fully proven.

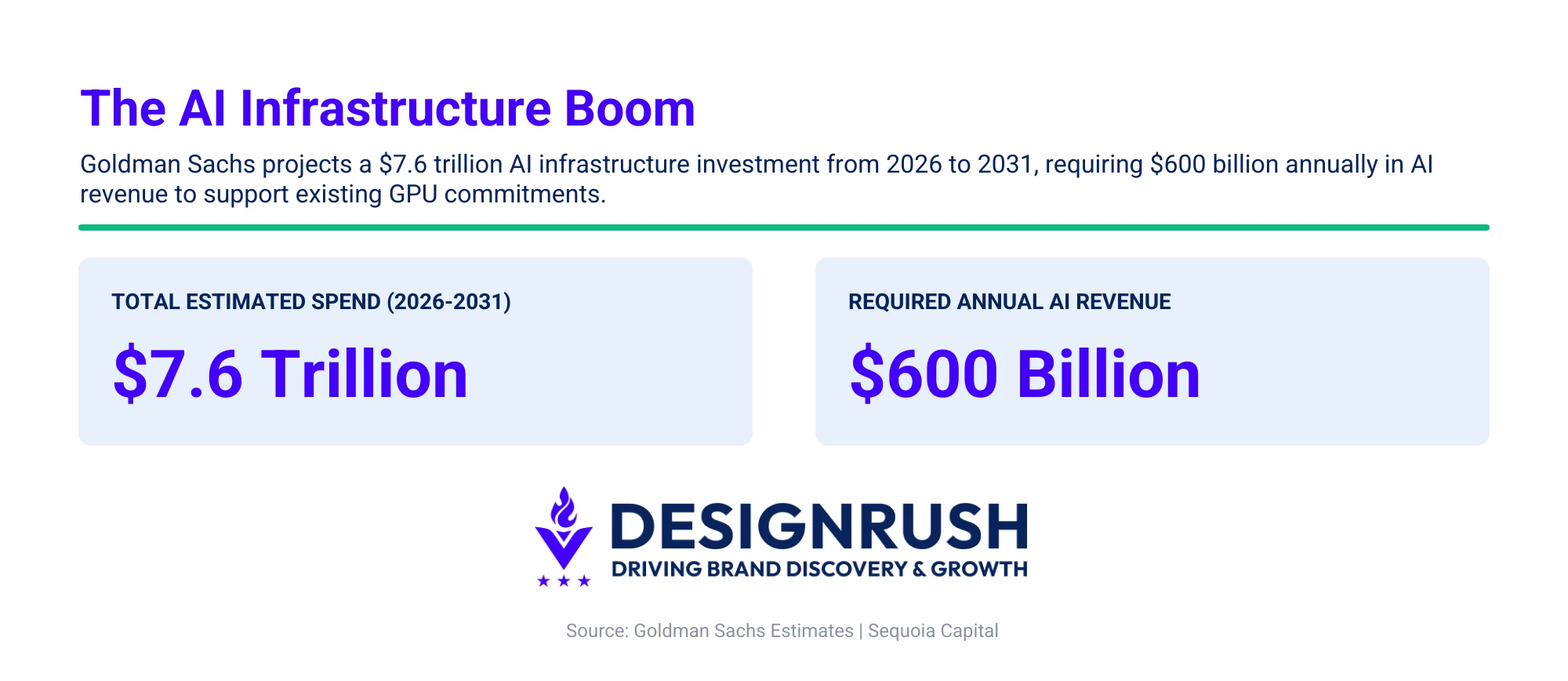

$7.6 trillion. That's Goldman Sachs' estimate for total AI infrastructure spend between 2026 and 2031 across GPUs, data centers, and power systems.

Sequoia Capital's AI revenue-gap analysis put the problem plainly:

The industry would need roughly $600 billion in annual AI revenue to support the GPU investment already committed. Revenue is growing quickly, but it has not yet caught up to the scale of the buildout.

That gap is what worries skeptics. If growth slows before revenue catches up, the pressure spreads to the lenders, infrastructure providers, and investors financing the expansion.

2. The Bull Case Counterpoint - Real Infrastructure, Real Revenue, and a Historical Precedent

The counterargument is structural rather than simply optimistic. It rests on $700 billion in committed capital, verifiable hardware revenue, and a historical pattern where the infrastructure outlasts the bubble.

More importantly, that spending is already translating into real revenue.

The Hardware Layer Is Already Generating Verifiable Revenue

NVIDIA's numbers are the clearest proof point: the company posted $215.9 billion in total revenue for FY2026, with data center revenue specifically reaching $193.7 billion, recognized sales from shipped hardware, not projected future value.

Across the Big Five hyperscalers, including Amazon, Microsoft, and Meta, capital expenditure is now forecast to exceed $600 billion in 2026, a 36% increase over 2025, with roughly 75%, or $450 billion, directly tied to AI infrastructure.

Enterprise Adoption Is Moving From Experimentation to Production

The demand side is expanding in parallel:

- McKinsey’s State of AI research found AI adoption reached 72% of organizations by 2025, up from 55% in 2023.

- Deloitte's 2026 State of AI in the Enterprise survey, covering 3,235 senior leaders, found that 66% of organizations reported productivity gains from AI, with worker access to the technology rising 50% in 2025 alone.

- The number of companies with 40% or more of their AI projects in production is set to double within six months (Deloitte).

The companies at the center of the cycle are converting that adoption into real revenue at scale:

- OpenAI surpassed a $20 billion annualized revenue run rate by the end of 2025.

- Anthropic reached roughly a $14 billion annualized revenue run rate in 2026.

- Databricks announced it crossed a $5.4 billion annualized revenue run rate with positive free cash flow.

The Infrastructure Precedent: Capital Destroys, But the Rails Remain

The infrastructure analogy also holds up historically. Both the railroad bubble of the 1800s and the dot-com crash both destroyed enormous amounts of investor capital, but the infrastructure built during those periods remained and later became economically foundational.

In fact, Amazon’s stock fell roughly 95% from its dot-com peak during the crash before later recovering to become one of the world’s most valuable companies.

Two data points suggest the current AI cycle, while large, has not yet reached the excess of prior bubbles:

- Current AI infrastructure investment sits at roughly 2% of U.S. GDP, below the railway boom's peak near 6% and the dot-com era's 1-2% in pure infrastructure terms

- Unlike the firms that collapsed in 2000, today's hyperscalers are financially stronger, with higher cash flows, sustained profitability, and resilience to absorb a correction without systemic failure, according to Goldman Sachs

Speaking at the World Economic Forum in Davos, NVIDIA CEO Jensen Huang framed this spending as: "the largest infrastructure buildout in human history," arguing that "we have to build the infrastructure necessary for all of the layers of AI above it."

He described AI as a "five-layer cake" spanning energy, chips, cloud data centers, models, and applications, with the application layer being where, in his words, "ultimately… economic benefit will happen."

Even if AI valuations correct, the companies selling foundational tools and technology capture the most consistent returns, and the infrastructure itself doesn't disappear.

3. The IPO Convergence: What Happens When Four Trillion-Dollar Companies Go Public

The clearest test of whether the current AI cycle is sustainable or speculative may come in late 2026 to 2027, when several of the world’s largest private AI companies are expected to hit public markets almost simultaneously.

Here is the anticipated pipeline. SpaceX has already listed (June 12); Anthropic (filed June 1) and OpenAI (filed June 8) have both submitted confidential S-1s and are targeting Q4 2026 to 2027 debuts:

Company | Expected Timing | Anticipated Valuation |

SpaceX | Public as of June 12, 2026 | ~$1.77T at IPO price (~$2.1T at close) |

Anthropic | October 2026 | ~$965 billion |

OpenAI | $852B-$1 trillion |

The convergence is already looking less simultaneous than expected: SpaceX has listed, but Open has signaled 2027, leaving Anthropic as the most likely of the giants to follow SpaceX into public markets this year.

Analysts describe 2026 as one of the most concentrated AI-driven IPO cycles in market history. SpaceX, OpenAI, and Anthropic alone could add roughly $3 trillion in combined market value to public markets.

Expected demand for the largest AI listings is already projected to rival or exceed the size of the recent U.S. IPO market.

The Risk: Private Valuations Meet Public Scrutiny

Public markets, however, are less forgiving than private ones because the underlying economics become visible all at once.

Early signs of caution are already emerging. Bloomberg has reported that after contacting hundreds of institutions, at least one firm found "not a single one was willing to buy OpenAI" on the secondary market.

This is a possible signal that private-market enthusiasm may not fully translate once these companies face public-market scrutiny.

The second half of 2026 will be the first real stress test of whether AI's private-market assumptions hold when the economics are fully visible.

What the Largest Startup Funding Rounds of All Time Tell Us

18 of the top 20 rounds on this list went to AI or AI-adjacent companies. Four companies raised 65% of all global venture capital in a single quarter.

History offers two outcomes from moments like this: the infrastructure outlasts the speculation and becomes the foundation of the next economic era, or the revenue never catches up to the commitments and public markets price the gap.

With SpaceX now public and OpenAI and Anthropic having filed within a week of each other, the second half of 2026 will be the first honest answer.

![]()

Our team ranks agencies worldwide to help you find a qualified partner. Visit our Agency Directory for the Top Business Consulting Firms as well as:

- Top Startup Consulting Firms

- Top Business Operations Consulting Firms

- Top Small Business Consulting Firms

- Top Consulting Firms in Columbus

Our design experts also recognize the most innovative design projects across the globe. Visit our Awards section for the best & latest.

Largest Startup Funding Rounds FAQs

1. What is the largest startup funding round ever?

OpenAI’s $122 billion private round, closed Q1 2026, is the largest on record. It was co-led by SoftBank alongside Andreessen Horowitz, D.E. Shaw Ventures, MGX, TPG, and T. Rowe Price Associates at an over $800 billion post-money valuation.

It surpassed OpenAI’s own March 2025 record of $40 billion, which had held for less than nine months.

2. What is considered a ‘mega-round’ in venture capital?

A private funding round of $1 billion or more. The threshold was historically rare, but now routine for AI companies.

A more meaningful distinction in 2026 is $5 billion, since rounds above that level are large enough to reshape category competition rather than just fund one company’s growth.

3. What is the difference between a funding round and a fund like the SoftBank Vision Fund?

A mega-round is capital raised by one company in exchange for equity or debt. The Vision Fund is an LP-funded investment vehicle: institutional investors committed capital to SoftBank, which then deployed it across dozens of companies.

SoftBank’s $100B never went to a single company. Instead, it was pooled capital for a portfolio. It’s on the list because no analysis of capital at this scale can omit a fund that reshaped the entire category.

4. How many unicorn startups exist today?

As of mid-2026, there are approximately 1,200 to 1,300 unicorn startups globally, according to Crunchbase and CB Insights estimates.

The count peaked above 1,200 in 2022, contracted slightly during the 2023-2024 valuation reset, and has grown again as AI valuations have expanded the pool.

The United States accounts for approximately 50% of the global unicorn count, followed by China, India, and the United Kingdom.

5. Which company has raised the most total venture funding of all time?

OpenAI has an estimated $165B+ in total external funding. No other private company comes close.

The next closest in cumulative raised are SpaceX+xAI (combined, post-merger) and Uber, both far behind.

6. What is the average size of a Series A, B, and C funding round in 2026?

Current benchmarks, based on 2025-2026 Crunchbase data:

- Series A funding rounds have a median of approximately $18-22 million. For context, some of the largest Series A funding rounds in AI have exceeded $100 million given compute cost requirements.

- Series B rounds typically range from $40-80 million.

- Series C rounds are broadly $100-300 million, with AI and infrastructure companies routinely exceeding $500 million.

These averages have increased substantially from 2018 baselines, reflecting both inflation and the higher capital intensity of AI workloads.