Q1 2026 was the largest venture quarter ever recorded. Of the $300 billion invested across roughly 6,000 startups, AI took $242 billion, leaving about $60 billion that didn't chase a model.

For agencies and brand leaders, this is more than market trivia. Freshly funded companies often use new capital to build go-to-market teams, reposition for growth, and outsource work they can't hire fast enough.

Knowing which sectors raised tells you where new business opportunities are emerging and which clients may soon face budget pressure.

Non-AI Startup Funding 2026: Key Findings

- Prioritize defensibility over features. Fintech attracted $12B and digital health $7.4B, but funding concentrated in companies with proprietary data, licenses, or hard-to-replicate assets.

- Capital is moving from software to physical systems. Nearly $4B went to defense autonomy alone, while semiconductor and robotics companies captured some of the largest non-AI rounds.

- Regulatory change can create billion-dollar opportunities overnight. Prediction markets raised $3.6B after favorable federal developments unlocked the category for institutional investors.

Who Should You Pitch in 2026? Matching Funded Sectors to Agency Services

1. Largest Startup Funding Rounds

2. How AI Broke Startup Funding

3. Most Anticipated IPOs of 2026

4. Startup Failure Rates

Our report serves as a guide to where 2026's new budgets are forming.

Use it to decide where to prospect, which funded companies to prioritize, and where your agency may be overexposed.

The headline-grabbing mega-rounds aren't where the opportunity sits. The U.S. deal funnel shows why (CB Insights, Q1 2026):

Round Size | Number of Deals | Capital Raised | Share of Total US Funding |

$500M+ | 31 | $232B | 80% |

$100M-$500M | 165 | $30B | 10% |

$50M-$100M | 162 | $11B | 4% |

$10M-$50M | 658 | $14B | 5% |

$1M-$10M | 1,020 | $4B | 1% |

Thirty-one deals at $500M or above captured 80% of total U.S. funding, roughly $232B, while the 1,020 deals between $1M and $10M, the broadest, most active slice of the market, split just 1%, or $4B combined.

The record quarter is a tall, narrow spike, not broad-based growth. That shape dictates three decisions:

- Where should you prospect next? The five sectors below absorbed most of the non-AI $60B. If your agency has credibility in defense, fintech, digital health, prediction markets, or advanced manufacturing, you're already close to 2026's newest budgets.

- Which prospects deserve attention first? The $100M-$500M band is the sweet spot: 165 companies with real capital to spend, growing faster than they can hire, and still building the marketing function that mega-round companies already have in-house.

- Where are you overexposed? Deprioritize the $1M-$10M cohort as they’re high effort, low budget. Traditional horizontal SaaS is another area to approach cautiously, as multiples have dropped from 7x to around 3.3x forward revenue.

One emerging trigger to watch: with IPOs still limited, companies approaching major financing, secondary sales, or IPO preparation often increase spending on communications, PR, and investor-facing branding.

What This Means for Different Service Providers

For each persona, the action is concrete:

- For agency owners: Defense, fintech, digital health, and advanced manufacturing companies just raised billions. Vertical expertise in a regulated category is now your strongest differentiator.

- For agencies serving SaaS clients: Expect budget pressure. With app software repriced, your SaaS clients are cutting spend. Shift conversations from acquisition to retention and efficiency before they shift them for you.

- For consultants and advisors: Regulatory change created a multi-billion-dollar category (prediction markets) almost overnight. Clients in regulated or soon-to-be-deregulated spaces need strategic guidance more than ever and will pay for it.

Now let's look at the data behind these insights.

The Short Answer: The $60B Went to Defense, Prediction Markets, Chips, and Smaller Bets

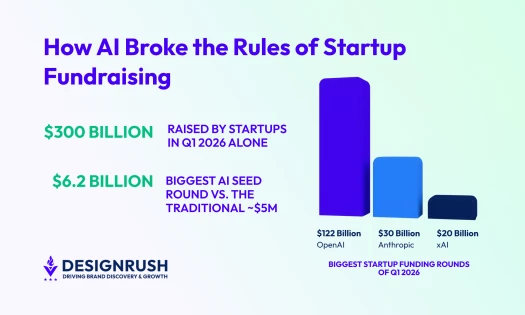

Four companies, OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and Waymo ($16 billion), raised $188 billion between them, close to two-thirds of the global total.

Strip out the rest of AI, and you’re left with the $60 billion the non-AI economy fought over. That’s only 20% of the dollars, but a far larger share of the companies.

Mega-rounds tell you what a handful of investors believe about the next decade, while the other 20% shows what the market is willing to fund today, on normal terms.

So, where did the money go?

- ~$3.75 billion went to two defense companies, Shield AI and Saronic, building autonomous weapons systems,

- Roughly $3B went to prediction markets, which is a category unlocked by federal regulation, not a product innovation

- Billions more went to chip foundries, robotics platforms, data-center infrastructure, and a bifurcating fintech sector. Most of it, as explained below, physically adjacent to the AI economy even when categorized differently.

Before the Breakdown: Most Non-AI Deals Are AI Infrastructure in Disguise

Before breaking down the $60B by sector, a transparency note: much of what appears to be non-AI capital is actually the physical infrastructure layer of the same AI cycle.

Cerebras builds chips for AI inference, NScale and DayOne supply AI compute, and Skild AI, NEURA Robotics, and World Labs are training physical systems on AI models.

These rounds sit in buckets like "robotics", "chips," or "data center" by category label, but they belong on the AI infrastructure map.

The $1B+ cohort reflects this:

Company | Amount | Sector |

Polymarket | ~$2B | Fintech/prediction markets |

DayOne | $2.0B | Data center infrastructure (APAC/Europe) |

Shield AI | $2.0B | Aerospace & defense |

NScale | $2.0B | AI compute infrastructure |

Global Technical Realty | $1.9B | Data center infrastructure (Europe) |

Saronic | $1.75B | Defense/autonomous ships |

Rapidus | ~$1.7B+ | Semiconductor manufacturing |

Skild AI | $1.4B | Robotics/physical AI |

NEURA Robotics | ~$1.2B | Robotics/physical AI |

Wayve | $1.2B | Autonomous driving |

Cerebras | $1.0B | Chips/AI compute |

Kalshi | $1.0B+ | Fintech/prediction markets |

World Labs | $1.0B | AI spatial intelligence/world models |

Below the $1B threshold, the remaining capital is diffused by nature:

- $12B across 762 fintech deals (Crunchbase).

- $7.4B across 336 in digital health, with biotech and enterprise software making up the rest (CB Insights).

With that framing in place, here's what the non-AI ~$60 billion actually funded and why each category got it.

Where the $60B (20%) Went: A Sector-by-Sector Breakdown

Most of the $60 billion landed in five sectors. Here's a breakdown of why each category earned its share:

- Defense autonomy captured nearly $3.75B as investors backed military hardware over software

- Prediction markets attracted $3B after regulatory wins triggered valuation surges

- Fintech led non-AI funding with $12B across 750 deals, but investors became more selective

- Digital health secured $7.4B as investors favored proprietary data and healthcare infrastructure

- Advanced manufacturing boomed as 40% of China's Q1 deals targeted chips, robotics, and industrial tech

1. Defense Autonomy Captured $3.75B as Investors Backed Military Hardware Over Software

If one sector defines the non-AI 20%, it's defense autonomy, and it's the clearest example of capital rotating from software into hardware with real revenue.

Two of the biggest deals came from defense startups:

- Shield AI, which develops autonomous military aircraft technology, raised $2 billion at a $12.7 billion valuation in March (Crunchbase).

- Just days later, Saronic, a company building autonomous surface vessels for naval operations, secured $1.75 billion at a $9.25 billion valuation (CNBC).

Together, those two rounds accounted for ~$3.75 billion in funding.

Both companies had real revenue before raising: Shield AI had just won a major contract from the U.S. Air Force. Both Shield AI and Saronic also attracted backing from large private equity investors with billions of dollars under management.

In H1 2026, defense-tech venture funding more than doubled in the first six months of 2026 to over $12 billion, eclipsing the roughly $10 billion the sector raised in all of 2025:

- Anduril anchors it, now in talks at a ~$100 billion valuation, up from $61 billion eight weeks earlier.

- Shield AI raised $1.5 billion in March

- Mach Industries quadrupled its valuation to $1.8 billion

- Europe's Helsing raised $1.8 billion at $18 billion.

The common thread is a shift toward cheaper, expendable "attritable" systems rather than the expensive-to-replace platforms that defined defense contracting for decades.

Agency takeaway: Defense startups flush with capital need employer branding, public-affairs-savvy communications, and B2G marketing – specialties few agencies offer. Less competition means premium rates for those who can navigate the space.

2. Prediction Markets Attracted $3B After Regulatory Wins Triggered Valuation Surges

Prediction markets are the standout category with zero AI involved.

The recent surge in investment follows a series of court victories and favorable regulatory developments that strengthened the case for prediction markets operating under federal oversight, making the sector look far more scalable to investors.

- Kalshi, a federally regulated prediction market where users trade contracts on future events, raised a $1 billion at a $22 billion valuation.

- Polymarket secured a $2 billion strategic investment from Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange, at an $8 billion pre-money valuation.

Agency takeaway: Newly legitimized categories spend heavily on trust. Prediction-market platforms need compliance-aware creative and PR that repositions them away from "gambling” – a rare greenfield for agencies.

3. Fintech Led Non-AI Funding With $12B Across 750 Deals, but Investors Became More Selective

Fintech remained the largest non-AI sector by dollar value, but investors became far more selective.

Capital flowed to companies with proprietary data, regulatory licenses, and financial infrastructure, while consumer apps and easily copied products saw less interest.

Crunchbase tracked roughly $12 billion into fintech across about 750 deals early in the year, with an average deal size of $22.5M (Crunchbase).

In fintech, defensibility is winning over features alone. The top fintech funding deals in Q1 2026 reflect this:

- Tala raised $500 million for its mobile lending platform, which relies on proprietary borrower data in underserved markets.

- World Liberty Financial raised $550 million in the crypto and DeFi sector.

- Devoted Health secured $317 million to expand its Medicare Advantage insurance business, a heavily regulated market with barriers to entry.

Agency takeaway: With investors funding defensibility over features, fintech briefs are shifting from growth-at-all-costs to credibility, regulatory positioning, and CAC efficiency.

For agencies, that creates demand for credibility-focused marketing. For software and product development firms, it creates opportunities to build infrastructure, integrations, security features, and compliance capabilities that make fintech harder to displace.

4. Digital Health Secured $7.4B as Investors Favored Proprietary Data and Healthcare Infrastructure

Digital health followed the same selective pattern as fintech. Investors favored companies with proprietary data, hardware, or deep healthcare integrations, and standalone software tools faced a tougher funding environment.

CB Insights tracked $7.4 billion across 336 deals in Q1 2026, with an average deal size of nearly $30 million.

The top digital funding deals in Q1 2026 are:

- Earendil Labs raised $787 million for drug development.

- Whoop raised $575 million for its fitness wearable platform.

Agency takeaway: Agencies that already understand HIPAA, FDA claims, and clinical-grade messaging can command premium rates.

For software and product firms, the opportunity is in building patient-facing apps, EHR integrations, data platforms, and security that help these platforms earn the trust of health systems.

5. Advanced Manufacturing Boomed as 40% of China's Q1 Deals Targeted Chips, Robotics, and Industrial Tech

Besides AI applications in Q1, investors also poured capital into the hardware and manufacturing systems needed to support them.

Across the quarter, roughly 18 semiconductor companies raised mega-rounds of over $100 million. Among the largest deals included:

- Cerebras raised $1 billion at a roughly $23 billion valuation as customers sought alternatives to the dominant GPU supplier.

- Rapidus secured about $1.7 billion to build a leading-edge semiconductor fabrication plant in Japan.

The trend is even more pronounced in China. According to IT Juzi’s database, advanced manufacturing accounted for roughly 40% of all funding deals in Q1, making it the country's largest venture category.

Capital flowed toward semiconductors, industrial robotics, AI systems, batteries, quantum computing, and commercial space.

Agency takeaway: As these businesses scale toward enterprise customers and public markets, many need positioning, technical content, and demand generation.

For development firms, the opportunity is in the work they can't easily hire for: specialized automation, integrations, and infrastructure that takes too long to build in-house.

When to Act: Reading the Signals That Come After the Round

A funding round creates an opportunity, but timing matters.

The best window is usually the first 30-90 days after a raise when budgets are being approved, and growth plans are underway, but internal teams are still understaffed. That's when companies are most likely to bring in outside partners.

The strongest buying signals tend to be the same across sectors:

- Hiring a first CMO or VP of Marketing often triggers a review of existing vendors and agency relationships.

- A product launch pushes teams to reassess partners after months focused on development.

- Rapid hiring in marketing, communications, or demand generation signals that growth plans are moving into execution.

- Preparing for an IPO or secondary sale typically increases spending on communications, investor-facing content, and brand positioning.

In regulated sectors, there's a second clock running alongside the funding one. License approvals, contract awards, and favorable regulatory rulings often unlock a second wave of spending, as the company is now permitted and motivated to invest in visibility.

The companies most worth prioritizing are the ones where multiple signals are firing at once: a recent round, a new marketing leader, and a regulatory milestone on the horizon.

Non-AI Venture Funding 2026: Final Words

The $60B that moved outside AI this quarter is where agencies and brand decision-makers have the most room to act. Mega-round companies often have mature marketing teams and established agency relationships, but the $100M-$500M band is still building all of that.

The sectors that captured the middle ground are entering a period where budgets are growing faster than internal teams. Vertical expertise, regulatory fluency, and speed of execution are the differentiators that win those mandates.

The window is open now, but it won't stay that way.

![]()

Our team ranks agencies worldwide to help you find a qualified partner. Visit our Agency Directory for the Top Business Consulting Firms as well as:

- Top Startup Consulting Firms

- Top Business Operations Consulting Firms

- Top Small Business Consulting Firms

- Top Consulting Firms in Columbus

Our design experts also recognize the most innovative design projects across the globe. Visit our Awards section for the best & latest.

Non-AI Venture Capital Funding 2026 FAQs

1. Why is Q1 2026’s venture capital so concentrated in AI?

Because a small number of investors believe that foundation models are a once-in-a-generation infrastructure bet, and they're writing increasingly large checks to secure that position.

North America saw a 190% increase in dollars deployed alongside a 26% drop in deal count. Mega-rounds of $100 million or more accounted for 86% of all global capital in Q1 2026, leaving 14% for every other stage and size. (CB Insights; Crunchbase)

2. Why did the deal count hit its lowest point since 2016 despite a record funding quarter?

Capital consolidated into fewer, larger rounds rather than spreading across more companies. The average U.S. deal reached $66.3 million in Q1 2026, while the median sat at just $4 million, a gap that shows how heavily the topline is skewed by mega-rounds.

Thirty-one deals at $500 million or above captured 80% of all U.S. funding; the 1,020 deals between $1 million and $10 million captured just 1%. (CB Insights, Q1 2026)

3. What is venture capital bifurcation?

Bifurcation describes a market that appears healthy in aggregate but has split into two very different experiences: well-funded winners raising large rounds on favorable terms, and everyone else finding the market thin, slow, and unforgiving.

In Q1 2026, bifurcation showed up most clearly in fintech and in the seed market (a16z).

4. What is the secondary market, and why does it matter for startup equity in 2026?

The secondary market covers transactions where existing shareholders sell their stakes before an IPO or acquisition, typically via tender offers, GP-led secondaries, or structured continuation vehicles.

It matters because the IPO window has only cracked open, and only for the very largest names — SpaceX listed in June, and Anthropic and OpenAI have filed — while for everyone below the mega-cap tier, a public exit remains effectively out of reach.

The M&A picture improved in Q2, with a record $113 billion in $1 billion-plus acquisitions, but that liquidity has concentrated at the top just as the funding has.

5. What happened to SaaS funding in 2026?

Traditional SaaS was repriced. Public application software now trades at roughly 3.3x forward revenue, down from a five-year average above 7x.

Horizontal software fell about 25% over the trailing twelve months, while vertical software fell 34% (Jefferies, Apr. 2026, via Foley & Lardner).

AI can now perform many of the tasks that some software companies previously charged thousands of dollars for. As a result, investors are placing less value on software that can be easily replaced.

6. How should non-AI founders position their startup when fundraising in 2026?

Lead with defensibility over TAM (Total Addressable Market). Proprietary data, regulatory licenses, or hardware integration will move investors faster than market size projections. Be ready to answer why a well-resourced AI lab couldn't replicate your product in six months.

Bring in corporate venture arms and strategics early, and plan for a longer process: with the median deal at $4M and deal count down 26% in Q1 (CB Insights), runway management matters more than it has in years.

7. What signals indicate a funded startup is ready to hire an agency?

The clearest signs a company is building its vendor roster are a first CMO or VP of Marketing hire, rapid marketing-team expansion, a major product launch, or preparation for a secondary sale or IPO.

In regulated sectors such as defense, fintech, digital health, and prediction markets, funding is only one trigger. A contract award, license approval, or favorable regulatory ruling often acts like a second funding event.