Corporate money now dominates the top of venture. Here's what that shift means for the priorities, timelines, and decisions of the companies that agencies and brands work with.

Corporate Venture Capital Funding: Key Findings

- Check investor type before pitching. Corporate VC now accounts for 50%+ of venture funding by dollars, often bringing longer approval cycles and more stakeholders.

- Research the parent company behind every corporate-backed startup. With 77% of Fortune 100 firms investing in startups, corporate priorities often shape buying decisions.

- Build expertise in strategic sectors. Corporate VCs backed 68% of AI deal value and are increasingly active in climate, defense, and manufacturing.

What a Startup's Investors Tell You Before You Pitch

1. Leading Venture Capital Firms

2. How AI Broke Startup Funding

3. Largest Startup Funding Rounds

4. Startup Failure Rates & Stats

A company's investors shape its priorities, its timelines, and who actually makes decisions.

A defining venture capital trend in 2026 has been a change in the kind of money behind startups. Corporations and large institutions now sit on cap tables that used to belong to independent venture firms.

Each type of investor has different priorities, and those priorities often show up in how the company buys.

For agencies, knowing the investor type is a qualification step that tells you who the real decision-makers are, how long the cycle will run, and how to frame what you pitch.

Here's what to look for and what to do with it.

- Identify the lead investor type, whether it’s Independent VC, corporate VC (CVC), or sovereign/institutional. This is usually public, either on their site, in funding announcements, or on Crunchbase.

- Match the backer to a likely priority:

- An independent VC lead is a financial-only investor whose only interest is growth toward an exit. The company is optimizing for metrics and the next round.

Pitch ROI, speed, and traction. Decision cycles tend to be faster. - A corporate VC lead is an investment arm of a larger company that wants both returns and strategic value. Research the parent company, as the startup's roadmap is likely shaped by what the parent needs.

Position your services around strategic fit, partnerships, or market expansion, and expect more stakeholders in the approval process. - A sovereign or institutional lead is where you expect more stakeholders, longer timelines, and attention to compliance, local presence, and the backer's broader agenda. Pure growth messaging is less likely to land on its own.

- An independent VC lead is a financial-only investor whose only interest is growth toward an exit. The company is optimizing for metrics and the next round.

- Look for corporate investors that could become prospects. If a Fortune 100 company is on the cap table, that corporation runs a venture program and is often a direct client in its own right. The startup connection is a warm angle in.

Now let's dig into the numbers to see why startup funding has changed and what different investors expect in return.

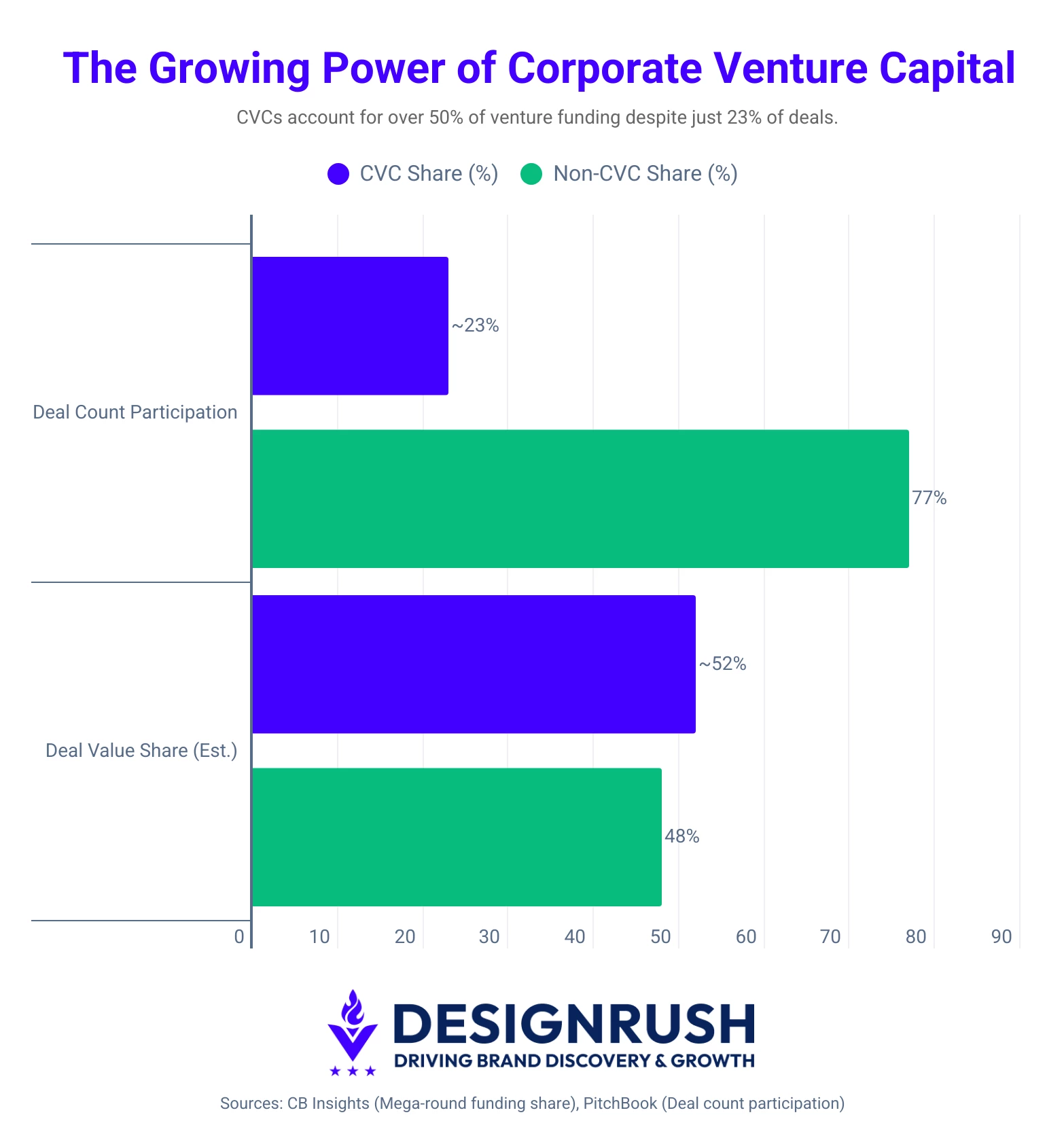

CVCs Account for Over 50% of Venture Funding Despite Just 23% of Deals

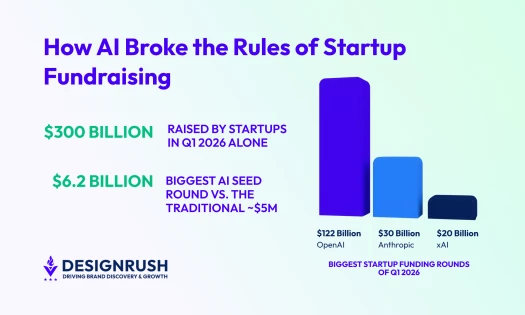

The biggest venture rounds of Q1 2026 came from corporations and institutional investors with strategic agendas that extend beyond financial returns.

aThe top five deals alone accounted for 73.2% of Q1 2026 US deal value, and the largest of them, OpenAI ($122B), Anthropic ($30B), xAI ($20B), and Waymo ($16B), were backed by names like Microsoft, Nvidia, Google, Temasek, the Qatar Investment Authority, and Abu Dhabi's MGX (Pitchbook).

Corporate venture capital now runs through a larger share of the market, most of it clustered at the top:

- Mega-rounds of $100 million or more made up 59% of all CVC funding (CB Insights).

- 22% of all VC globally flows through corporate venture arms, up from 15% three years ago, with corporate deployment projected to clear $28 billion in 2026 (NVCA/Spectup).

Yet corporate VCs participate in only ~23% of US venture deals by count, but a far larger share by dollars (PitchBook). Traditional VC still dominates by deal count and at the early stages, where most companies live.

The pattern has only continued past Q1. A single late-June funding day saw Menlo Ventures, Goldman Sachs Alternatives, BlackRock, UBS Investment Bank, Aramco Ventures, Khosla Ventures, and Norwest all writing checks within the same 12-hour window.

Corporate, sovereign, and institutional money cluster at the top of the market, exactly where the dollars have concentrated all year.

Traditional VC vs. Corporate VC: What It Means for Startup Companies

Here's the single most useful question to ask before working with any funded company: What does their money want?

Their reasons differ, and that shapes the company you end up working with.

Traditional VCs Are No-Strings-Attached Investments

A traditional VC has one mandate: financial return. Its only real interest is the company growing on its own toward an exit.

The question it's asking is: "Can this become a $10 billion company?" It usually works on a 5-to-7-year clock, measures success in exits, and carries no agenda beyond the money.

With an independent VC, the startup’s founder is often the real decision-maker you have to deal with.

Corporate VCs Invest for More Than Financial Returns

A corporate VC has two mandates. Alongside the return, it's asking, "Can this become useful to us?" Corporations also weigh things a financial investor never would, like manufacturing efficiency, distribution reach, and competitive defense.

The upside for the funded company is access to technical resources and the parent's distribution, and the validation that comes with a big-name backer.

The catch is that corporate money carries an unspoken expectation to build something the investor already wants.

How Corporate Money Came to Dominate the Top of the Market

This shift happened in three steps: traditional VC pulled back, corporations stepped in, and institutional capital filled the gap at the top.

- Traditional VC pulled back due to lack of cash returns

- 77% of Fortune 100 companies now invest in startups; mostly to track innovation

- Large institutional funds stepped in where traditional VC couldn't

1. Traditional VC Pulled Back Due to Lack of Cash Returns

Traditional ventures' biggest problem is the distribution drought or lack of cash returns.

Many funds raised during the last cycles have generated paper gains but returned little cash to investors, meaning most LPs are still waiting to see most of their money back.

The median 2017-vintage fund had returned just 0.27x of the capital its investors put in after eight years, while 2021-2022 vintage funds are sitting at 1.0-1.2x total value with near-zero cash distributions as of 2025.

Thus, LPs are becoming more selective. Many have stopped committing new capital to new funds until the existing ones return.

The pullback has affected smaller firms the hardest:

- At the 2021 peak, venture firms with under $250 million in assets raised $23.1 billion across 506 funds in the US (Financial Times).

- By mid-2025, it had collapsed to just $1.41 billion across 27 funds.

- In 2025, 30 firms raised 75% of all the capital that went into US venture funds, with nine firms taking in half the total (PitchBook)

- The squeeze runs through the fund layer too: institutional LPs put 91% of new Q1 2026 commitments into established, brand-name firms, a record high, up from 74% for all of 2025.

This reflects fewer new relationships and far less tolerance. Founders face a market with fewer independent funds and a growing presence of corporate and institutional capital looking towards firms with real, realized returns.

What this means for agencies: A company backed by a 2021 or 2022 vintage fund may be working with an investor under quiet pressure to show returns. That pressure travels downstream.

It's worth understanding before you walk into a retainer conversation, because the growth budget at that company may be tighter.

H1 2026 data hardened the pattern: 16 megafunds raised nearly 70% of the $72.4 billion committed to US venture funds, funds over $1 billion took roughly 72% of all capital raised, and first-time managers accounted for under 10%, while LPs stayed cautious (PitchBook-NVCA Venture Monitor).

2. 77% of Fortune 100 Companies Now Invest in Startups; Mostly to Track Innovation

Corporations stepped into the gap traditional VC left, but they’re not doing it solely to make money:

- Today, 77% of Fortune 100 companies now engage in some form of venture investing: accelerators, CVC arms, and partnership vehicles (CB Insights).

- A record 65% of corporate venture deals are now early-stage, even though the bulk of their dollars still lands in those big $100 million-plus rounds (CB Insights).

But they mostly don’t buy the companies they back. Fewer than 4% of CVC-backed companies are acquired by their corporate backers, and that figure has been stable since 2000 (PitchBook).

Instead, corporations are buying visibility. CB Insights frames CVC explicitly as a "market-sensing mechanism", which is a cheap, early seat at the table to watch technologies or business models before they become threats or opportunities.

In other words, corporations invest in what they need to understand, and occasionally in companies they may one day buy.

What this means for agencies: A Fortune 100 company running a venture program is signaling where it expects change to happen next.

If your agency has credibility in a sector that corporation is actively funding, you've got a natural conversation starter with both the startup and the corporate investor behind it.

3. Large Institutional Funds Stepped In Where Traditional VC Couldn't

Sovereign wealth funds collectively manage more than $12 trillion in assets globally, giving them the ability to write billion-dollar checks and support capital-intensive projects at a scale beyond what most traditional venture or private-equity funds can deploy.

In the first eight months of 2025 alone, large institutional funds put $46 billion into AI. Some of the clearest corporate venture capital examples come from the biggest rounds of 2025-2026:

- Temasek, Singapore's state investor, in OpenAI

- The Qatar Investment Authority in Anthropic

- Abu Dhabi's MGX and Mubadala scaling up AI bets across 2025 and 2026.

Looking Ahead: Where Strategic Capital Goes Next

The shift toward corporate is a change that's still unfolding. Among the venture capital trends worth watching are two in particular: where traditional VC is retreating, and how capital concentration is reshaping the companies that continue to get funded:

- Strategic capital may flow to sectors traditional VC avoid

- The question is shifting from who funds you to what they want in return

- The corporate money itself is now under pressure

1. Strategic Capital May Flow to Sectors Traditional VC Avoid

Corporations are moving into sectors that a cautious VC market has left wide open to create strategic industrial partnerships with founders and startups:

- CVCs participated in 68% of overall AI deal value in 2025 (Bain & Company)

- Climate tech Series B deals fell 29% while deal sizes also shrank by 28%, creating what analysts have named a "missing middle", which is the capital gap between a working technology and the first commercial-scale deployment

The same dynamic is playing out in defense tech and deep biotech. These sectors all need patient capital, and traditional VC's 5-to-7-year clock increasingly can't provide it.

Corporate and sovereign investors, however, don't have that constraint.

Agency takeaway: Sectors like climate, defense, and deep bio are often under-resourced on brand and marketing because growth-stage capital has been scarce.

Build credibility in one now, and you'll be well-positioned when companies in the sector begin expanding beyond product development and into go-to-market investment.

2. The Question Is Shifting From Who Funds You to What They Want in Return

More venture capital is flowing to fewer companies:

- The top 1% of startups captured 33% of all US VC dollars in 2025, up from 12% in 2022 (Silicon Valley Bank).

- Only 15.5% of seed-stage companies funded in Q1 2023 had reached Series A by Q1 2025 (Cambridge Associates).

Capital-intensive startups in AI infrastructure, climate hardware, defense, and advanced manufacturing may have to rely on strategic investors, as traditional VC may not be willing or able to fund them all the way to scale.

Agency takeaway: The biggest rounds now come with more complex investor relationships. That can be a qualification signal, as more strategic investors involved means more stakeholders and competing priorities, and a longer path to approval.

3. The Corporate Money Itself Is Now Under Pressure

The strategic capital filling venture's funding gap comes from corporate balance sheets that are spending on AI faster than they earn:

- Across the July 2026 earnings round, Amazon guided to roughly $220 billion of AI spending this year, Microsoft signaled it would about match the $190 billion it spent over the prior twelve months, and Meta raised its 2026 capital spending guidance to $130B-$145B.

- Alphabet's free cash flow turned negative on $118 billion of quarterly revenue - the first time in its history as a public company.

- Meta's free cash flow fell to $784 million on $61 billion of revenue, with its Reality Labs division losing nearly $9 billion in the first half of 2026.

Most of that spending goes into AI infrastructure, but it still shapes startup funding.

Through July 2026, investors sharply rewarded and punished the same spending depending on the return: Microsoft reached a six-month high because of its AI investments. Meanwhile, Meta fell to near a one-year low after announcing AI products with no timeline attached.

That pressure travels downstream. A corporate venture arm whose parent is defending its own capex to shareholders is a less patient investor than the same arm was a year ago.

Agency takeaway: Check what a startup's corporate parent said about AI returns on its most recent earnings call. If the parent is under pressure to show results, the companies it backs will inherit that urgency.

Expect shorter proof windows, harder questions about measurable outcomes, and less appetite for long brand-building engagements. Conversely, a parent that just demonstrated returns (Microsoft's position) is more likely to keep funding exploratory work.

Corporate Venture Capital Funding: Final Words

The shift from traditional to corporate venture capital is a map of where priorities, decisions, and budgets are moving, and agencies that read it early will pitch smarter and qualify faster.

Know who's behind the money, understand what they want in return, and you'll walk into every conversation with a clearer picture of what the company actually needs to buy.

![]()

Our team ranks agencies worldwide to help you find a qualified partner. Visit our Agency Directory for the Top Business Consulting Firms as well as:

- Top Startup Consulting Firms

- Top Business Operations Consulting Firms

- Top Small Business Consulting Firms

- Top Consulting Firms in Columbus

Our design experts also recognize the most innovative design projects across the globe. Visit our Awards section for the best & latest.

Corporate Venture Capital FAQs

1. What is corporate venture capital, and how is it different from traditional VC?

Corporate venture capital (CVC) is an investment arm run by an established company like Google Ventures or Intel Capital. These back startups for both a financial return and a strategic benefit to the parent.

Traditional VC is a financial-only investor: an independent fund whose single job is returning capital to the people who funded it.

For agencies working with corporate-backed companies, the practical upshot is that the parent's strategic priorities often shape what the startup builds and buys, sometimes more than the founder's own plan does.

2. Who is funding the biggest startups in 2026?

Mostly corporate and sovereign capital. The largest rounds of early 2026, including OpenAI, Anthropic, xAI, and Waymo, collectively raised $188 billion, backed by investors such as Microsoft, Nvidia, Google, Temasek, and the Qatar Investment Authority.

Traditional VC still leads by deal count, but at the top of the market, the money increasingly comes with a parent company or a national mandate attached.

3. Is traditional venture capital dying?

Contracting, not dying. The number of active small VC funds has dropped sharply; sub-$250 million firms raised $23.1 billion at the 2021 peak, and just $1.41 billion by mid-2025.

But total venture dollars are at record highs, driven by corporate and sovereign money filling the gap at the top.

4. Which sectors are corporate VCs most active in right now?

AI, overwhelmingly. Corporate VCs took part in 68% of all AI deal value in 2025, and AI's share of corporate venture deal value reached 94.6% in 2026.

Beyond AI, corporate money is active in defense tech, advanced manufacturing, and climate hardware, which are sectors with longer development timelines that traditional VC has grown reluctant to fund past the early stage.

5. How much of venture capital actually comes from corporations?

About 22% of all venture capital globally now flows through corporate venture arms, up from 15% three years ago.

By deal count, corporate VCs appear in only around 23% of US deals, but by dollars, they account for more than half of venture funding, concentrated in the biggest rounds.

Mega-rounds of $100 million or more made up 59% of all corporate venture funding in Q1 2026.

6. Why do corporations rarely acquire the startups their venture arms invest in?

Corporate venture capital works mainly as a market-sensing mechanism, an early, low-cost seat at the table to watch emerging technologies, rather than an acquisition pipeline.

That's why fewer than 4% of CVC-backed companies are bought by their corporate backers: most of the strategic value comes from the knowledge and relationships built during the investment, not from owning the company.

A corporate backer means credibility and access, but it rarely means a buyer is waiting in the wings.