SpaceX has already kicked off the year's biggest IPO wave, with Anthropic expected to follow as OpenAI weighs a 2027 listing. Together, the three companies are worth more than an estimated $3 trillion.

Here's what every investor needs to know about the best upcoming IPOs before the next window opens.

Upcoming IPOs To Watch: Key Findings

- Watch AI infrastructure. SpaceX, OpenAI, Anthropic, and Cerebras account for roughly 88% of the valuation represented on this list.

- Read the lockup terms in every S-1 filing, as insider share sales can significantly affect post-IPO performance.

- Don't ignore the quieter names. Companies like Stripe, Plaid, and Anduril may offer stronger fundamentals than some of the year's most heavily hyped listings.

Everyone's Watching the AI IPOs. What Else Is Coming?

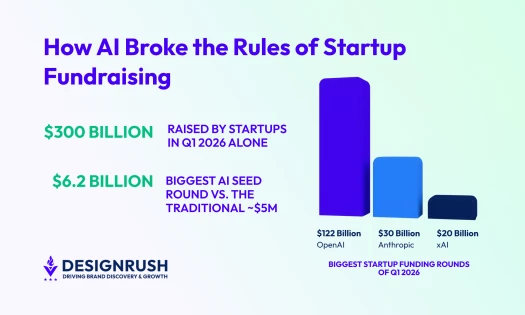

1. Largest Startup Funding Rounds

2. Largest IPOs of All Time

3. Leading Venture Capital Firms

4. Startup Failure Rates & Stats

The 2026 IPO calendar is the most concentrated capital event in a decade.

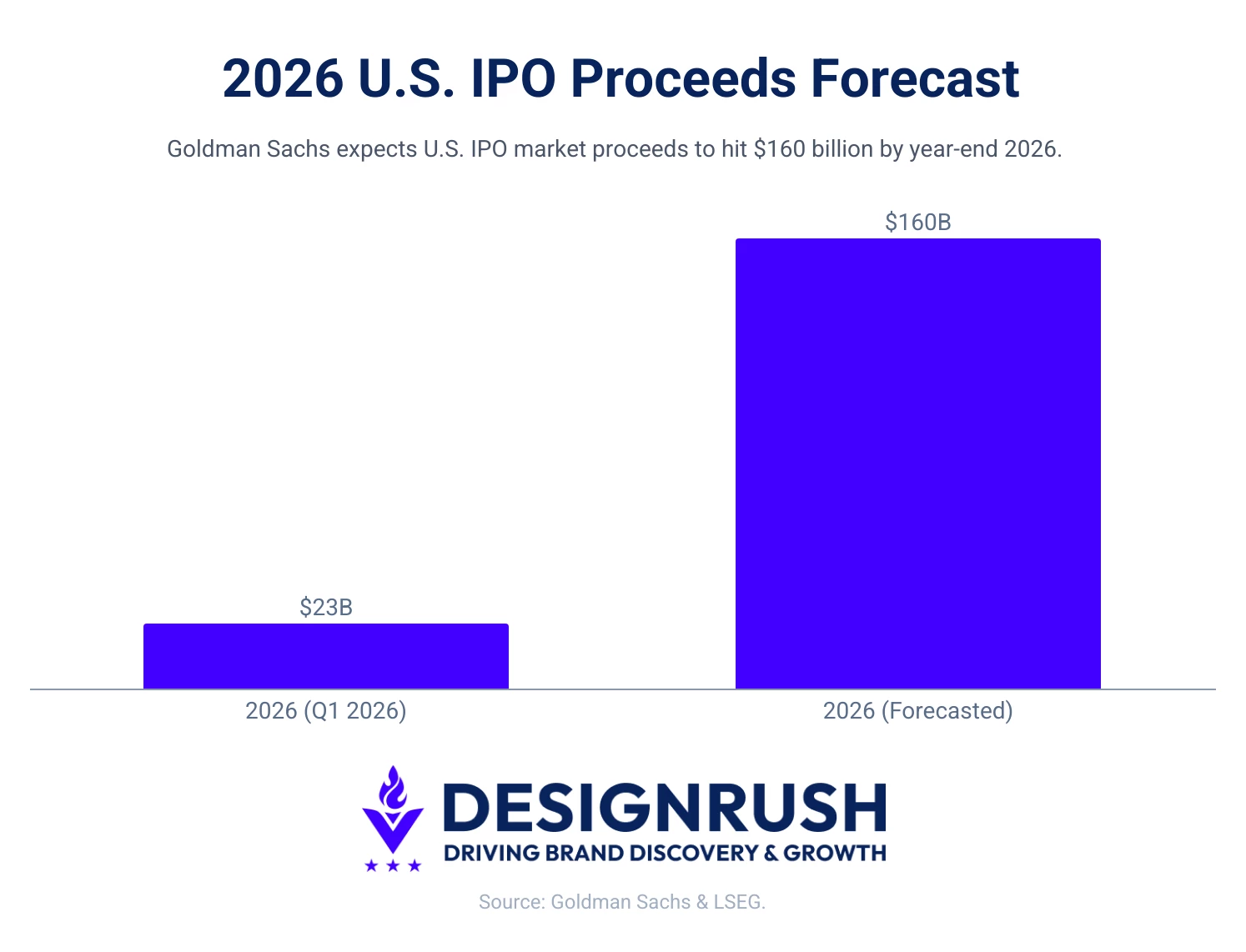

Goldman Sachs forecasts roughly $160 billion in U.S. IPO proceeds in 2026, potentially a record year.

U.S. markets have already absorbed $23 billion in IPOs in Q1 2026, a 91% jump year over year, with the mega-deals still ahead.

Much of that capital is expected to flow into AI and AI infrastructure. OpenAI, Anthropic, SpaceX, and Databricks are all moving toward public markets at around the same time, which is unprecedented.

But focusing only on the AI giants misses the bigger opportunity. Some of the most important IPO candidates of 2026 sit outside the headlines, from fintech infrastructure and defense technology to consumer platforms and e-commerce.

And as investors learned from Figma in 2025, a heavily hyped pre-IPO but not the top performer, the most talked-about name isn't always the one that ends up delivering the best return.

So while AI is attracting most of the attention, the better question is: what else is coming? Which is exactly what our list answers.

2026 Most Anticipated IPOs at a Glance

# | Company | Sector | Est. Valuation | Filing Status | Expected Debut |

1 | Aerospace/AI/Connectivity | ~2T | Public | Completed | |

2 | Artificial Intelligence | $852B-$1T+ | Confidential S-1 Filed | Possibly delayed to 2027 | |

3 | Artificial Intelligence | $965B | Confidential S-1 Filed | Oct. 2026 (target) | |

4 | Telecom/Digital | $135B-$180B | DRHP filed with SEBI | Aug-Oct. 2026 | |

5 | Fintech/Payments | $159B+ | No S-1 Filed | Late 2026-2027 | |

6 | AI Chips | $56B IPO Value ($95B Close) | Public (May 2026) | Completed | |

7 | E-Commerce | $30B-$50B | HKEX Filing Submitted | 2026 (TBD) | |

8 | Defense Technology | $61B | No S-1 Filed | TBD | |

9 | Consumer Software | $15B-$25B | Confidential S-1 Filed | 2026 (TBD) | |

10 | Fintech Infrastructure | $8B+ | No S-1 Filed | 2026-2027 |

1. SpaceX - The $85.7 Billion IPO That Broke Every Record

- Expected valuation: ~$2T

- Exchange: Nasdaq (ticker: SPCX)

- Status: Public as of June 12, 2026

The SpaceX IPO was one of the largest stock market events in recent history, vaulting the company into America's most valuable companies on day one.

Goldman Sachs led the underwriting alongside Morgan Stanley, Bank of America, Citigroup, and JPMorgan across a 21-bank syndicate.

SpaceX priced at $135 per share and raised roughly $85.7 billion, the largest IPO in history. Shares opened at $150 and closed at $161.11, up about 19%, carrying the market cap past $2 trillion.

The weeks since have been a round trip. Shares ran to an all-time high of $225.64 on June 16, a valuation near $2.77 trillion that briefly made Musk the world's first trillionaire, then fell to $147.11 by June 23 as a global AI selloff took hold.

The slide has since carried below the starting line. SPCX hit an all-time low of $145.07 on July 10, under its IPO-day close, and trades in the low $140s as of July 13, barely above its $135 offer price.

The next catalyst is August 6. SpaceX's first public earnings report and the first insider lockup release, when about 20% of insider shares become saleable, another 10% conditional on price triggers, and the remainder unlocking in stages through December 2026.

SpaceX claims a total addressable market of $28.5 trillion, larger than the entire European economy, though less than $2 trillion of that figure comes from space or connectivity. The remaining ~$26 trillion is tied to AI.

Three Risks Still Buried in the S-1

- Musk has total control. He holds around 82% of the voting power, meaning shareholders have almost no say in how the company is run. Buying SPCX is a financial bet on Musk, not a seat at the table.

- Retail investors receive unusually broad access to the IPO, with up to 30% of shares reportedly reserved for individuals through platforms such as Schwab, Fidelity, Robinhood, SoFi, and E*TRADE.

- A Tesla merger is on the table. Speculation about combining SpaceX and Tesla has grown ahead of the listing. The two companies already share board members, engineers, and hundreds of millions in annual transactions.

The bull case for SpaceX is Starlink, which has no real competitor, as nobody else has the satellites, the launch costs, or the regulatory approvals to match it. If subscriber growth holds and the next generation of rockets delivers, SpaceX could eventually grow into its price tag.

The bear case is that Starlink customers fell 18% to about $81/month between 2023 and 2025, as the company expands into lower-priced international markets.

M&A appetite is also reshaping the company. The xAI merger already adds exposure to a $250 billion AI business that is still losing money, and days after listing, SpaceX announced the $60 billion all-stock Anysphere (Cursor) acquisition – the largest startup acquisition ever.

For shareholders, it means dilution and a faster-than-advertised pivot toward AI, and the announcement was among the catalysts investors cited for the stock's slide from its peak.

2. OpenAI - Can a $1 Trillion Valuation Outrun Massive AI Costs?

- Expected valuations: $852B-$1T+

- Exchange: Nasdaq (expected)

- Status: Confidential S-1 filed June 8, 2026

- Debut Target: Reportedly weighing a delay from 2026 to 2027

OpenAI moved toward a confidential IPO filing shortly after SpaceX's IPO plans emerged, with Goldman Sachs and Morgan Stanley helping lead both offerings. The timing seems deliberate: watch how the market receives SpaceX, then price accordingly.

In late June, the New York Times reported that the company is considering delaying its listing until 2027 to give itself a better shot at a $1 trillion valuation, citing SpaceX's slide from its post-IPO peak as a cautionary reference point.

The bull case is that enterprise adoption is accelerating, with OpenAI’s annualized revenue hitting ~$25 billion as of February 2026 and targeting $600 billion in total compute spending by 2030.

If OpenAI can convert its brand recognition and early lead into durable long-term contracts before rivals close the technology gap, the revenue trajectory could eventually justify the price.

The bear case is what it costs to get there.

OpenAI posted a $38.5 billion net loss for 2025 on $13.07 billion in revenue, projects roughly $14 billion in further losses for 2026, and has disclosed infrastructure commitments totaling about $1.4 trillion.

OpenAI does not expect to become cash-flow positive until 2029, with HSBC estimating a $207 billion funding gap by 2030 even after projected revenue growth.

Competition from Google and Anthropic is real and well-funded. Gemini's share of AI web traffic grew from 5.7% to 21.5% over the past 12 months while ChatGPT's fell from 86.7% to 64.5%, per Similarweb.

3. Anthropic - The Enterprise AI Challenger Growing Faster Than Its Rivals

- Expected valuations: $965B

- Exchange: Nasdaq (expected)

- Status: Confidential S-1 filed June 1, 2026

- Debut Target: October 2026 (reported)

Of the big three AI companies going public this year, Anthropic filed first, confirming a confidential S-1 on June 1, 2026, beating OpenAI to the SEC by a week. Yet it still aims to debut last, targeting October.

That combination is the advantage: it locks in optionality early while letting Anthropic watch where SpaceX and OpenAI land before pricing, so it can decide exactly how aggressive to be.

On May 28, Anthropic closed a $65 billion Series H, pushing its post-money valuation to $965 billion and making it the most valuable private AI company in the world — then filed to go public four days later.

Anthropic makes Claude, the AI model increasingly favored by large enterprises. Roughly 80% of its revenue comes from business customers, and the number spending more than $1 million annually doubled to over 1,000 less than two months after its February 2026 funding round.

The bull case: Anthropic has the fastest enterprise revenue growth of the three.

Its annualized run-rate climbed from roughly $10 billion at end-2025 to $14 billion in February, $30 billion by April, and $47 billion by May.

The company has also told investors it expects its first profitable quarter with a run-rate above $50 billion within weeks.

The bear case: The compute bills are enormous and locked in for years. Anthropic is paying SpaceX $1.25 billion per month, roughly $15 billion a year, for access to data centers and GPU capacity through May 2029.

Earlier this year, a dispute with the U.S. government also temporarily disrupted access to its most advanced Claude models before the restrictions were lifted in June.

The episode ended largely in Anthropic's favor, but it previews exactly the kind of regulatory risk factor its S-1 will have to disclose.

The company is also facing two consumer lawsuits – a class action over Claude Max usage limits and a $75 million copyright suit brought by authors – adding to its pre-IPO legal overhang.

4. Reliance Jio - India's Largest-Ever IPO Finally Files

- Expected valuations: $135B-$180B

- Exchange: NSE & BSE (India)

- Status: DRHP filed with SEBI on June 19, 2026

- Debut Target: Q3 2026 (Aug-Oct, pending SEBI review)

After six years of speculation, the largest IPO in India's history is officially in motion. On June 19, 2026, Mukesh Ambani confirmed that the board of Jio Platforms had approved its Draft Red Herring Prospectus and filed it with SEBI, BSE, and NSE.

Jio is the digital, telecom, and AI arm of Reliance, with a user base above 524 million and the world's largest fixed-wireless broadband footprint.

Crucially, banks are increasingly valuing it as a tech platform rather than a telecom; the premium rests on its payments, media, broadband, and sovereign-AI ambitions.

The bull case: Jio sits at the center of India's digital consumption super-cycle and carries marquee global backers from its 2020 raise. At ~$140 billion, it would instantly rank among India's two or three most valuable listed companies.

The bear case:The tiny ~2.5-2.9% float means a small supply of shares meeting heavy demand, which can drive sharp early volatility. The valuation also leans on digital and AI optionality that has yet to fully show up in revenue, and the listing remains exposed to SEBI's review timeline.

5. Stripe - The $159 Billion Fintech Giant That Still Doesn't Need an IPO

- Expected valuations: $159B+

- Exchange: Nasdaq (expected)

- Status: No S-1 filed

- Debut Target: Late 2026, possibly 2027

Stripe has been "about to IPO" since 2021. CEO Patrick Collison has been consistent that Stripe does not need public-market capital and can remain private for as long as it makes sense, showing little urgency to pursue an IPO.

Stripe processes payments for more than five million businesses. In 2025, those businesses ran $1.9 trillion through their platform, up 34% from the year before.

At $159 billion, Stripe is already priced at a significant premium to PayPal, its closest public comparable, which processes similar volumes but trades at a fraction of that number.

Stripe has also become the payments infrastructure for the AI economy. OpenAI, Anthropic, Perplexity, and Mistral use Stripe's payments and billing tools as they turn AI products into subscription businesses.

The bull case: Stripe is profitable, growing fast, embedded in both traditional e-commerce and the emerging AI economy, and run by a founder known for making good decisions slowly. It is the most operationally sound company on this list.

The bear case: Apple, Shopify, and the major banks are all building their own payment infrastructure, which puts pressure on the fees Stripe charges and the share of the market it can hold.

And unlike a software company, payments volume is tied to the broader economy, so a consumer slowdown hits Stripe directly, with little buffer.

6. Cerebras Systems - The AI IPO That Tested Investor Demand

- IPO valuation: $56B (at offer price) / ~$95B (at close)

- Exchange: Nasdaq | Ticker: CBRS

- Status: Public as of May 14, 2026

- Raised: $5.55 billion

For investors asking which is the best IPO to buy now, Cerebras is another name on this list already trading.

It was priced at $185 and closed its first day at $311.07, up about 68% - a debut that looked like proof of bottomless demand for AI infrastructure, and the largest U.S. tech listing since Uber in 2019.

Six weeks later, that read looks premature. The stock had fallen more than 40% from its first-day high, trading around $200 by late June.

Its first earnings report as a public company, on June 23, showed revenue up about 92% year over year but guided gross margin down to 36-38% from 47%, and shares fell roughly another 10%.

Cerebras was supposed to be the tell for how the market would greet SpaceX and the wave behind it. The signal was a huge first-day appetite, followed by a sharp repricing once the lockups, customer concentration, and margin math came into view.

The bull case: OpenAI signed a ~$20 billion deal to buy computing capacity from Cerebras for ChatGPT, while AWS is also deploying Cerebras chips in its data centers. The company says its capacity is effectively sold out through 2027.

The stock has begun recovering in July, jumping 12% in a session on plans to expand US production capacity sevenfold with Flex and open its first European data center.

The bear case: The revenue is dangerously concentrated. About 86% of 2025 revenue came from two UAE-affiliated customers, and the backlog is nearly 80% reliant on OpenAI.

Nvidia's software ecosystem also remains deeply entrenched, and switching costs cut against Cerebras as often as for it.

7. Shein - A $38 Billion Retail Giant Still Searching for an Exchange

- Expected valuations: $30B-$50B

- Exchange: Hong Kong (expected)

- Status: Confidential filing submitted to HKEX, July 2025

- Debut Target: 2026 (unconfirmed)

Shein has been trying to go public for over two years. It failed in New York, stalled in London, and is now pursuing Hong Kong, its third attempt. This is because the business is large enough to list, but too politically contested to list anywhere convenient.

Its business model: Shein’s algorithm can turn social media trends into small production runs in as little as three days, compared with several weeks for traditional fast-fashion retailers such as Inditex's Zara.

That speed propelled Shein to ~$38 billion in revenue in 2024, cementing its position as one of the world's largest fast-fashion companies.

Why Shein's Third IPO Attempt May Be Its Hardest Yet

- China remains the key risk. Despite its Singapore headquarters, Shein's China-based supply chain and reliance on Beijing's approval process have complicated its IPO plans.

- Forced-labor allegations tied to Xinjiang continue to hang over the company. Shein denies them, but the scrutiny has already complicated multiple listing attempts.

The bull case: Shein would trade cheaply relative to its $38 billion in revenue, a fraction of Inditex's, which owns Zara, multiple despite faster growth.

The bear case: Pressure is coming from every direction: tariffs, trade barriers, supply chain scrutiny, and Beijing's veto over any listing. Valuation has already collapsed from $100 billion to $30-50 billion in three years.

8. Anduril Industries - Defense Tech's Fastest-Rising IPO Candidate

- Expected valuation: $61 billion

- Exchange: Nasdaq (expected)

- Status: No S-1 filed

- Debut Target: TBD (no confirmed timeline)

Anduril is one of the fastest-growing defense companies in the United States in under a decade. It raised $5 billion in May 2026 at a $61 billion valuation, a funding round led by Thrive Capital and Andreessen Horowitz, more than doubling its valuation from $30.5 billion less than a year earlier.

Its founder, Palmer Luckey, has said publicly that Anduril will "definitely" go public, and that there is no realistic path to winning the kinds of trillion-dollar defense contracts the company is pursuing without being publicly traded.

No S-1 has been filed, and no timeline has been confirmed.

Anduril's Growth Depends on One Customer: The U.S. Government

- Anduril's business is heavily dependent on U.S. government contracts, which is reliable but concentrated. A shift in defense priorities, a change in administration, or a budget dispute in Congress can reprice those contracts overnight.

- The proposed Golden Dome missile-defense program is the highest-profile example. Securing a major role is an advantage, but it also ties the company's future to political outcomes investors cannot reliably predict.

The bull case: Defense budgets are rising, and drone warfare is central to modern conflict. If Lattice becomes the standard software backbone for autonomous military systems, it could significantly expand Anduril's addressable market.

The bear case: The concentration of revenue from one customer: the US government. Contracts can be reversed, procurement delayed, and budgets frozen.

9. Discord - A Huge Audience Still Waiting to Pay Off

- Expected valuations: $15B-$25B

- Exchange: Nasdaq

- Status: Confidential S-1 filed January 2026

- Debut Target: 2026 (originally Q1; timing uncertain)

Discord filed confidentially for its IPO in January 2026, working with Goldman Sachs and JPMorgan. A March debut was the original target, but the listing has not materialized on that schedule.

The company has 200 million monthly active users, famously rejected a $12 billion acquisition offer from Microsoft in 2021, and has been building toward public markets ever since.

Discord started as a gamer chat tool and expanded into a general-purpose community platform. The core product is free. Revenue comes primarily from Nitro, a $10/month subscription for better streaming, custom emojis, and larger uploads.

The company is working to diversify revenue beyond Nitro through digital goods and developer-focused monetization tools.

Discord: Can 200 Million Users Become a Bigger Business?

- The valuation gap from the 2021 funding round is worth noting. Discord was valued at $15 billion in 2021. Today, estimates still sit around $15-25 billion despite years of growth and revenue gains.

- Child safety is also a material risk: Discord faces lawsuits over minor exploitation, and its new CEO testified before Congress. Expect this to dominate the S-1.

The bull case: Discord has 200 million monthly users and revenue has doubled in two years with limited monetization. If it can expand advertising or business tools without alienating users, there is significant upside.

The bear case: Discord's users are resistant to commercialization. Passionate free communities rarely monetize cleanly.

10. Plaid - The Fintech Infrastructure Behind the AI Economy

- Expected valuations: $8B+

- Exchange: Nasdaq (expected)

- Status: No S-1 filed

- Debut Target: 2026-2027 (timing uncertain)

Plaid is infrastructure. Most people have never heard of it, but anyone who has linked a bank account to Venmo, Chime, or Betterment has probably used it.

Its core product is a data connection layer that lets third-party apps access bank account information securely, without the user handing over sensitive credentials directly.

The company connects consumer bank accounts to more than 11,000 financial institutions and thousands of apps. A February 2026 funding round valued it at roughly $8 billion, primarily to provide employee liquidity, often a signal that IPO preparations are underway.

Its CEO has confirmed an IPO is on the roadmap, while its CFO says the company has "earned the right to pick its time."

The bull case: Revenue grew 40% in 2025 to over $500 million, accelerating from 27% the prior year (WSJ). Its use case has also expanded from a connectivity layer into fraud detection, payments, mortgage verification, and onboarding.

The bear case: Plaid depends on access to bank data that it does not control. JPMorgan has publicly challenged the economics of that relationship, pushing for fees on aggregators such as Plaid and raising concerns about data access and security.

Honorable Mentions: 4 High-Profile IPOs Still Taking Shape

These companies aren't expected to headline the 2026 IPO calendar, but they're still among the most closely monitored private businesses by investors worldwide:

1. Revolut | Expected Valuation: $200B | Debut Target: 2028

Revolut is Europe's most valuable startup and has no immediate plans to go public.

CEO Nik Storonsky confirmed in April 2026 that a listing is at least two years away, and a November 2025 secondary share sale at a $75 billion valuation reduced the pressure further by giving existing investors partial liquidity.

When it does list, the target range is a valuation of $200 billion, which would rank among the largest fintech listings ever.

The business supports that ambition on paper: $6 billion in revenue in 2025, $2.3 billion in pre-tax profit, 52.5 million customers, and a full UK banking licence finally secured in March 2026 after a four-year wait.

2. Canva | Expected Valuation: ~A$65B | Debut Target: 2027

The Australian design platform confirmed it will not IPO in 2026. Co-founder Cliff Obrecht told reporters the company is "fully IPO ready" but wants its shift toward AI and workflow tools to be established before facing public market scrutiny.

Canva has made a series of acquisitions, including Affinity and Leonardo.Ai, as it expands from a design platform into broader workplace productivity and AI tools, putting it on a collision course with Microsoft and Google's productivity suites.

3. Kraken| Expected Valuation: TBC | Debut Target: 2026 (timing uncertain)

The US crypto exchange confirmed its confidential S-1, first filed in November 2025, remains active despite pausing IPO plans in March amid weaker market conditions.

Kraken is the most credible pure-play crypto exchange IPO candidate in the US, better regulated and more institutionally trusted than most of its peers.

The filing will force transparency on a sector that has operated largely without it, and the numbers Kraken puts in the open will set a benchmark for how public markets value crypto infrastructure.

The timing depends heavily on market conditions and whether the current regulatory environment holds.

4. Databricks | Expected Valuation: $134B | Debut Target: Likely 2027

The most financially conventional name in the AI pipeline has quietly stepped back from a 2026 listing.

Databricks crossed a $5.4 billion revenue run rate as of February 2026, growing 65% year-over-year with positive free cash flow, and closed a $5 billion round at a $134 billion valuation.

But on June 4, CEO Ali Ghodsi called 2026 "a terrible year to go public," pointing to the crowded SpaceX/OpenAI/Anthropic calendar and broader market turmoil, and signaled a likely 2027 debut.

Sector Breakdown: Most 2026 IPO Capital Is Flowing Into AI

Most of what’s going public in 2026 is essentially one big bet on AI. Here’s the map out of the pipeline by sector:

- ~88% is AI & AI infrastructure: SpaceX via Starlink and xAI, OpenAI, Anthropic, Databricks, Cerebras, and Anduril's Lattice AI platform

- ~4% is fintech: Stripe & Revolut

- ~5% is consumer, SaaS & e-commerce: Canva, Discord, & Shein

- ~2% is defense technology: Anduril's core defense-systems revenue

Compare that to 2021, when IPO money was spread across software, biotech, electric vehicles, fintech, and crypto. This year, it's almost all AI.

That's not necessarily bad, but it does mean that if sentiment around AI turns sour, every single name on this list gets hit at the same time.

Late June proved the point: AI-chip stocks fell across the board, SpaceX round-tripped, and several private AI companies delayed their IPO plans.

5 Forces Behind the Biggest IPO Wave in 2026

The 2026 IPO calendar is the convergence of six forces that have been building since 2021.

Together, they explain why the IPO window is reopening now, and why it could close just as quickly if market conditions change.

- Figma's post-IPO collapse made lockup schedules impossible to ignore

- Private markets can no longer fund AI's biggest companies alone

- AI is expensive, more expensive than anyone planned

- After five years of waiting, venture investors need liquidity

- Investors are done paying for stories: From AI hype to proving the business works

1. Figma's Post-IPO Collapse Made Lockup Schedules Impossible to Ignore

The biggest mistake in 2025's IPO was lockup engineering.

When a company goes public, early investors and employees are typically barred from selling their shares for a set period, usually 90 to 180 days. When that window opens, a flood of supply can hit the market, pushing the price down.

Figma is the most recent example. Figma’s stock fell 80%+ from its post-IPO peak because its unlock schedule released shares in multiple separate waves, each one hitting just as the previous sellers were finishing.

The lesson for 2026: find out when insiders can sell before you buy. SpaceX, OpenAI, and Anthropic will each have that schedule buried in their filings. A stock that looks fairly priced on day one can look very different six months later when millions of additional shares hit the market.

2. Private Markets Can No Longer Fund AI's Biggest Companies Alone

For years, the private market delayed IPOs by giving companies the option of secondary sales and giant private funding rounds, avoiding the public eye entirely.

That arrangement is breaking down. Companies like SpaceX, OpenAI, and Anthropic now require so much capital and have so many early investors waiting for liquidity that staying private indefinitely no longer makes financial sense.

Building AI data centers, satellite networks, and next-generation chips costs hundreds of billions of dollars. At this scale, the IPO market is reopening because some of the world's largest private companies have simply outgrown the private market.

Renaissance Capital projects 200-230 IPOs in 2026 raising $40-$60 billion. Goldman Sachs is more bullish, projecting around $160 billion in total U.S. IPO proceeds.

3. AI Is Expensive, More Expensive Than Anyone Planned

Morgan Stanley estimates that Amazon, Microsoft, Alphabet, Meta, and Oracle could collectively spend more than $800 billion on AI infrastructure in 2026 alone, with spending still climbing afterward.

The same banks estimate that the technology sector may need to issue as much as $1.5 trillion in new debt over the next several years to finance AI infrastructure and data-center construction.

For the startups trying to compete with them, they fall behind without access to that kind of capital. Going public is how infrastructure-scale businesses like OpenAI, Anthropic, and SpaceX close that gap.

4. After Five Years of Waiting, Venture Investors Need Liquidity

Many venture funds that backed today's biggest AI companies during the 2020-2021 boom need liquidity and an eventual return. That wait has stretched to five years or more.

The PitchBook-NVCA Q1 2026 Venture Monitor shows the median distributions-to-paid-in ratio for the past decade's vintages still sits below 1x, meaning many funds haven't even returned the original capital their LPs put in.

The pension funds, university endowments, and family offices behind those venture funds are now pressing for actual cash. SpaceX, OpenAI, and Anthropic going public represent the largest cash-out event in venture capital history.

5. Investors Are Done Paying for Stories: From AI Hype to Proving the Business Works

In 2021, a compelling vision was enough to command a billion-dollar valuation. That era is over. Investors going into 2026 want to see actual revenue, healthy profit margins, and a credible path to making money.

The companies that will succeed in this IPO cycle those that can back up the pitch with numbers. The ones that can't will find public market investors less forgiving than the private backers who funded them to this point.

That said, disagreement exists about how much of the current AI excitement is justified. Several prominent investors and analysts like Michael Burry have drawn comparisons to the dot-com bubble of the late 1990s.

Adjusted for inflation, the SpaceX, Anthropic and OpenAI IPOS will raise as much or more than the 300 internet and TMT IPOs did in 2000. $SPCX#Anthropic#chatGPT#SpaceX#openaipic.twitter.com/8hM8g1zxlw

— Cassandra Unchained (@michaeljburry) May 27, 2026

Others, including BlackRock CEO Larry Fink, contend that the AI boom is supported by real cash flows and earnings growth, distinguishing it from past technology bubbles that relied more heavily on future expectations.

Both camps are looking at the same data and reaching opposite conclusions, which is itself worth keeping in mind before committing capital to any of the names on this list.

Most Anticipated IPOs of 2026: Final Words

Three trillion dollars in private capital going public at the same time is a stress test for markets, for valuations, and for investors who haven’t seen an IPO wave this large in years.

Some names, like Databricks and Stripe, have the numbers to back up their valuations. Others are asking investors to pay for future potential.

And while AI will dominate the headlines, the infrastructure companies behind them may quietly outperform the ones commanding the most media oxygen.

2026 could be a historic year for IPOs, but also one where the gap between price and value is unusually wide. Know what you're buying, and read the S-1.

![]()

Our team ranks agencies worldwide to help you find a qualified partner. Visit our Agency Directory for the Top Business Consulting Firms as well as:

- Top Startup Consulting Firms

- Top Business Operations Consulting Firms

- Top Small Business Consulting Firms

- Top Consulting Firms in Columbus

Our design experts also recognize the most innovative design projects across the globe. Visit our Awards section for the best & latest.

Most Anticipated IPOs 2026 FAQs

1. What is the biggest IPO expected in 2026?

SpaceX was the biggest IPO of 2026 and the largest in history, raising $85.7 billion in June at an IPO-price valuation near $1.77 trillion.

OpenAI's listing could approach that valuation if it proceeds, but on raise size, SpaceX holds the record.

2. When did the SpaceX IPO happen?

SpaceX priced on the night of June 11, 2026, at $135 per share and began trading on the Nasdaq under SPCX on June 12. It closed day one at $161.11, up about 19%, raising roughly $85.7 billion in the largest IPO on record.

3. What is OpenAI's expected IPO valuation?

OpenAI is targeting a valuation between $852 billion and $1 trillion, with a confidential S-1 filed on June 8, 2026.

A September 2026 IPO window has been reported, but OpenAI itself cautioned that a listing "may be a while." As a result, the timeline remains uncertain, and some reports suggest the IPO could slip to 2027. At the upper end of its target range, OpenAI would become the largest pure-technology IPO in history.

4. Is Anthropic going public in 2026?

Anthropic confidentially filed for an IPO on June 1, 2026, days after closing a $65 billion Series H at a $965 billion post-money valuation, surpassing OpenAI as the most valuable private AI company in the world.

A public offering expected to raise more than $60 billion is targeted for October, with Goldman Sachs, JPMorgan, and Morgan Stanley reported to be in underwriting discussions.

5. What is the difference between a grey market IPO price and the actual IPO price?

The grey market is an unofficial pre-IPO market where speculative contracts trade before a company lists. Prices reflect expectations rather than real supply and demand, and frequently diverge from where the stock ultimately prices.

In 2026, this carries an additional legal risk worth understanding. Anthropic publicly declared shares sold through certain unauthorized secondary platforms void and unrecognized on its cap table, crashing funds that had marketed that exposure to retail investors.

The same transfer restrictions exist in OpenAI's shareholder agreements. Buying pre-IPO shares through a third-party platform may mean your shares have no legal standing when the company lists.

6. How to buy IPO shares in 2026?

There are three ways to buy into a 2026 IPO, each with a different entry point and risk level:

- Primary allocation: Submit an Indication of Interest through a participating broker, like Schwab, Fidelity, Robinhood, SoFi, or E*TRADE. The SpaceX S-1 confirms retail access through all five. Odds are low on hot deals, though; most buyers end up at the opening price anyway.

- Secondary market: Buy on day one at the opening price. You pay more, but you're trading on real demand, not speculation.

- Post-lockup: Insiders can't sell for 90–180 days after listing. When that window opens, prices often drop. Figma is the recent proof. Waiting frequently beats rushing in.

7. Are 2026 IPOs overvalued?

By traditional metrics, yes. SpaceX's proposed valuation equates to roughly 56x revenue and 109x EBITDA, outstripping Palantir and Tesla, two of Wall Street's priciest names, by a wide margin.

OpenAI is reportedly priced at roughly 25-30x forward revenue with significant operating losses. The bull case is that AI-economy growth will outpace any historical comparison; the bear case is that 2025's Figma-style post-lockup collapses will repeat.

8. How do I read an S-1 filing?

Focus on six sections in this order:

- Risk Factors - the lawyers' candid version of the bear case;

- Use of Proceeds - where the cash goes;

- Capitalization - post-IPO share count and dilution;

- Lockup Agreements - when can insiders sell;

- MD&A and Financial Statements - revenue growth, margin trajectory, accumulated deficit;

- and Related-Party Transactions - cross-company deals with founder-affiliated entities.

The full S-1 will be available on SEC EDGAR free of charge.