Headlines can tell you that artificial intelligence (AI) is growing, but they don’t tell you which functions are seeing revenue gains, which companies are scaling faster, or why many organizations still struggle to move beyond pilots.

We’re solving that here by bringing together 200+ AI statistics for 2026 across ROI, productivity, maturity, adoption, barriers, and budgets, giving you a clearer way to benchmark the market and separate momentum from measurable business results.

Artificial Intelligence Statistics: Key Findings

- 88% of organizations now use AI, yet 37% still apply it only at a surface level with little or no process change.

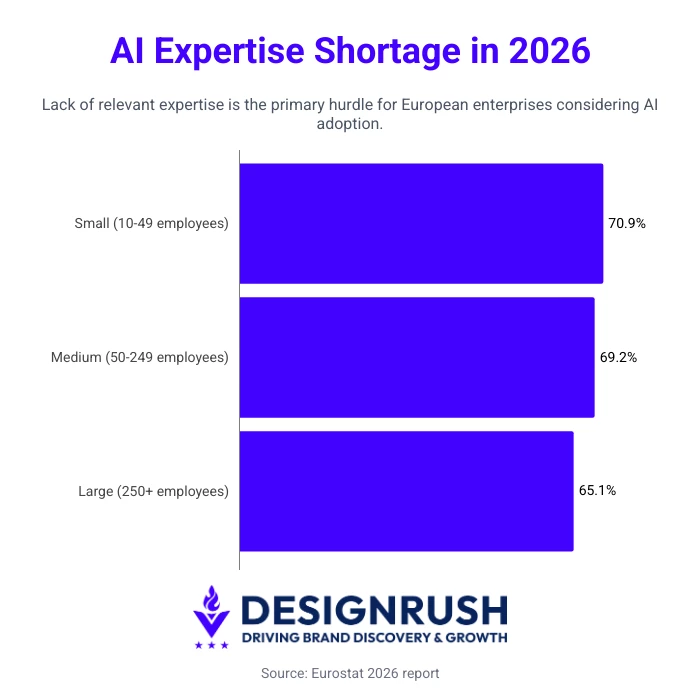

- Among companies that considered AI but did not adopt it, lack of expertise was the top obstacle for 70.9% of small enterprises, 69.2% of medium enterprises, and 65.1% of large enterprises.

- Worldwide AI spending is projected to reach $2.52 trillion by the end of 2026, up 44% year over year, with $1.37 trillion going to infrastructure alone.

Why 2026 AI Data Matters More Than AI Hype

AI is now widespread enough that broad adoption numbers no longer say much on their own. What matters is where AI is creating measurable gains, which companies are scaling faster, where maturity still falls short, and what barriers continue to slow results.

That is exactly what the artificial intelligence statistics in this article help clarify.

They give you a way to move past generic momentum claims and benchmark AI through the numbers that matter most to business decisions: revenue impact, cost reduction, productivity, operational maturity, adoption patterns, and investment direction.

How AI Is Affecting Revenue, Costs, and Productivity

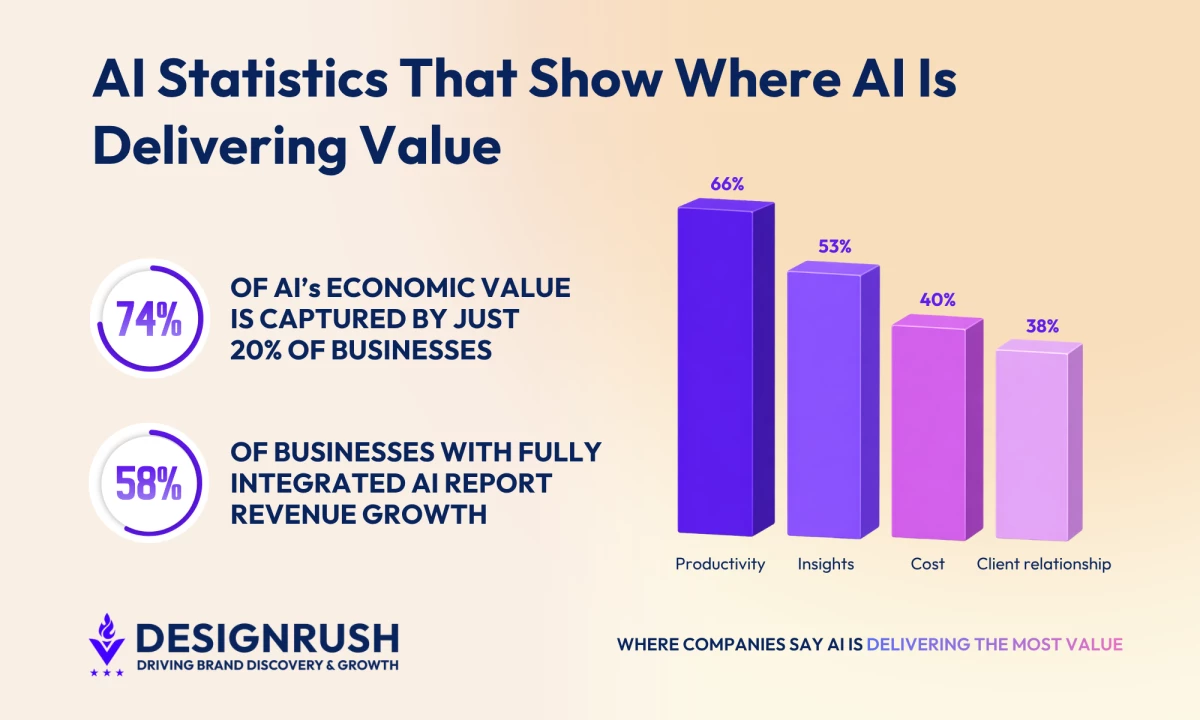

Only 20% of Organizations Report Revenue Gains From AI, While 74% of the Value Goes to the Top 20%

The 2026 data points to a clear conclusion: AI is delivering business value, but most of that value is still concentrated among a small group of organizations.

Productivity and efficiency gains are now common, while measurable revenue impact remains far less widespread.

- Productivity gains are showing up first in structured work

- Efficiency gains are common, but revenue gains still trail behind

- AI maturity has a major effect on financial outcomes

- The economic value of AI is highly concentrated

- How to move from AI pilots to profitable performance

Productivity Gains are Showing Up First in Structured Work

Stanford’s 2026 AI Index shows that productivity improvements are strongest in structured tasks, which helps explain why some functions are proving value faster than others.

Stanford’s 2026 AI Index shows that productivity improvements are strongest in structured tasks, which helps explain why some functions are proving value faster than others.

- 15% productivity gains in customer support

- 26% productivity gains in software development

- 50% increase in marketing output

Gisele Lempert Acosta, Co-Founder of Optimiza Vende Más, says AI is already becoming part of day-to-day business operations, from more personalized customer experiences and predictive insights to the automation of repetitive work.

She adds that when companies apply it well, AI can lower costs, improve efficiency, and strengthen competitive advantage.

Efficiency Gains Are Common, but Revenue Gains Still Trail Behind

Deloitte’s 2026 data shows that operational and decision-making benefits are much more common than direct revenue gains today.

- 66% report productivity and efficiency gains

- 53% report better insights and decision-making

- 40% report cost reduction

- 38% report better client or customer relationships

- 20% report innovation or product improvement

- 20% report revenue increase

- 74% say they expect AI to drive revenue growth in the future

AI is already helping many businesses work faster, reduce friction, and improve decisions, but only a smaller share can point to revenue growth already happening.

AI Maturity Has a Major Effect on Financial Outcomes

Grant Thornton’s 2026 survey shows one of the clearest maturity-to-value gaps available this year.

Grant Thornton’s 2026 survey shows one of the clearest maturity-to-value gaps available this year.

- 58% of organizations with fully integrated AI report AI-driven revenue growth

- 15% of organizations still in the pilot stage report AI-driven revenue growth

That makes fully integrated organizations nearly four times more likely to report revenue gains than those still experimenting.

The Economic Value of AI is Highly Concentrated

PwC’s 2026 AI Performance Study reinforces the same message from another angle. The value AI creates is real, but it is not evenly distributed.

- 74% of AI’s economic value is captured by just 20% of organizations

This means a relatively small group of companies is pulling ahead in turning AI into measurable financial results, while many others are still stuck at the stage of efficiency improvements, isolated use cases, or early experimentation.

How To Move From AI Pilots to Profitable Performance

A practical way to respond to this is to treat productivity, cost, and revenue as separate stages of AI value.

- Start by measuring AI in structured workflows where time savings and output gains are easiest to prove.

- Then track whether those operational gains improve margins, speed to market, conversion, retention, or another business result that leadership already cares about.

If the 2026 data shows anything clearly, it is that pilots and partial adoption do not produce the same outcomes as full integration.

You should separate experimental use cases from operational ones, prioritize the workflows where AI already shows measurable performance gains, and build from those results outward.

AI Adoption by Industry and Where Growth Is Spreading Next

AI Adoption by Industry Is Accelerating, With Retail Reaching 91% Engagement and Healthcare Hitting 70% Active Use

Retail, telecom, healthcare, and finance are all moving forward, but they are doing so at different speeds and with different definitions of success.

Some industries are already linking AI to revenue, cost reduction, and productivity gains, while others are still working through ROI uncertainty, skills gaps, and operational integration.

- Retail is one of the most commercially mature AI sectors

- 42% of shippers want AI-enabled logistics

- Finance is adopting AI steadily, with efficiency and analytics leading the way

- Telecommunications is moving from adoption to measurable performance gains

- Healthcare adoption is rising, but the value story varies by segment

Retail Is One of the Most Commercially Mature AI Sectors

NVIDIA’s retail data shows that the sector is already using AI across digital commerce, back-office operations, supply chain functions, and physical stores, with especially strong momentum around revenue and cost outcomes.

- 91% of the retail industry is engaged with AI

- 58% are actively deploying AI solutions, up from 42% in 2024

- 33% are currently assessing AI solutions

- 89% say AI is helping increase annual revenue

- 95% say AI is helping decrease annual costs

- 91% say AI is helping reduce annual supply chain costs

- 90% expect AI investment to grow in 2026

- 58% say that increase will be more than 10%

Retail’s strongest current AI use cases are concentrated in the parts of the business where efficiency and margin gains are easiest to prove.

Retail’s strongest current AI use cases are concentrated in the parts of the business where efficiency and margin gains are easiest to prove.

- 61% use AI in digital commerce

- 54% use it in back-office operations

- 45% use it in supply chain

- 24% use it in physical stores

AI agents are also moving into practical operational roles rather than staying confined to experimentation.

- 59% use AI agents for internal workflow automation

- 59% use them for knowledge management and retrieval

- 48% use them for customer support assistants

- 48% use them for employee assistants

- 48% use them for marketing and advertising

42% of Shippers Want AI-Enabled Logistics

AI adoption in logistics is moving forward, but most companies are still in the early stages.

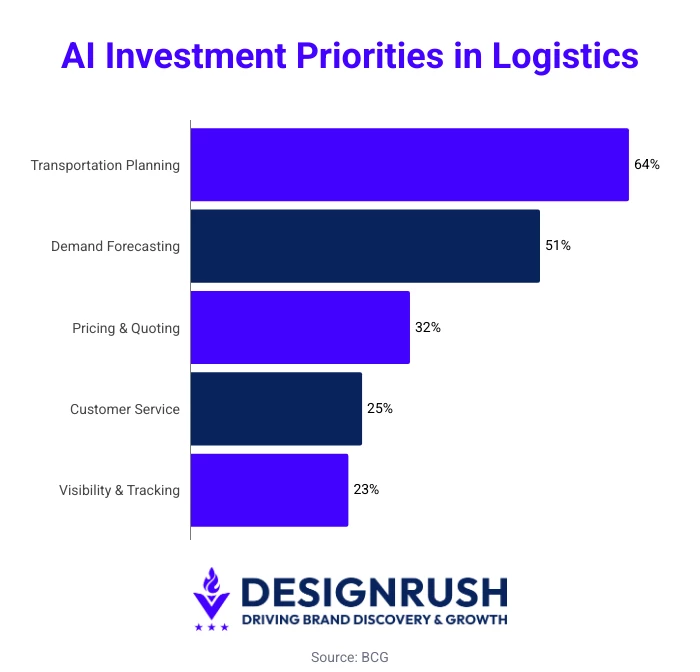

The BCG data points out that logistics leaders are investing in AI where planning quality, operational visibility, and cost control have the most immediate business impact.

Many companies have started exploring use cases, but far fewer have reached the point where AI is embedded in core workflows and tracked as a measurable contributor to performance.

The strongest investment priorities sit close to day-to-day execution. Companies aren't chasing abstract AI ambition. They're targeting areas where faster decisions and better predictions directly affect cost and service.

Top investment priorities:

- Transportation planning and execution: 64%

- Demand and capacity forecasting: 51%

- Pricing and quoting: 32%

- Customer service: 25%

- Visibility and tracking: 23%

Transportation planning leads because it sits at the center of route efficiency, resource use, and delivery performance.

Forecasting follows because capacity mismatches and inaccurate demand signals create avoidable cost fast.

Most Companies Are Still Early

Despite strong interest, maturity is limited. Half of shippers are still in the exploration phase, and only 1% say AI is embedded in core operations.

The logistic service providers (LSPs) are further along, but embedded adoption remains rare even there.

Current stage of AI adoption:

Phase | LSPs | Shippers |

Exploration phase | 30% | 50% |

Identified use cases | 26% | 17% |

Scaling applications | 23% | 25% |

Tracking AI contribution | 8% | 7% |

AI embedded in core operations | 13% | 1% |

The gap between interest and execution is the defining challenge for the sector right now.

A good example of how that gap can be closed comes from Unico Connect’s work with its client Ashokraj Transport & Logistics.

The company used a multilingual AI voice agent to turn WhatsApp voice-note orders in Hindi and English into structured, validated orders, showing how AI can take friction out of a repeated logistics workflow when the use case is clear and ready for production.

For logistics companies still trying to move from exploration to execution, that kind of narrow, production-ready application is often a more realistic starting point than a broad transformation program.

Cost Reduction Is the Primary Driver

Companies are pursuing AI primarily to lower costs, strengthen digital operations, and respond to competitive pressure.

AI Adoption Driver | LSPs | Shippers |

Cost reduction | 76% | 81% |

Corporate digital strategy | 30% | 45% |

Competitive pressure | 38% | 27% |

Automation | 29% | 27% |

Shippers also place more weight on digital strategy, which suggests AI is increasingly being treated as part of broader operational modernization.

LSPs show slightly more pressure from competition and customers, which fits their service-driven business model.

The Most Active Use Cases Share a Common Thread

The use cases gaining the most traction all sit close to operational decisions that affect time, cost, and service quality.

Use Cases | LSPs | Shippers |

Transportation planning and execution | 65% | 51% |

Visibility and tracking | 50% | 58% |

Demand and capacity forecasting | 44% | 48% |

AI earns its place fastest when it's embedded in a workflow that already carries operational weight.

- Planning affects route efficiency and resource allocation.

- Visibility affects customer communication and disruption management.

- Forecasting affects capacity, staffing, and inventory coordination.

Three Barriers Are Slowing Progress

The barriers help explain why so many companies remain stuck between interest and execution. Most already have a sense of where AI could help.

The harder part is proving business value, building internal capability, and integrating AI into existing systems.

Key Adoption Barriers | LSPs | Shippers |

Unclear ROI | 36% | 45% |

Lack of internal expertise | 37% | 40% |

System integration | 38% | 25% |

High implementation cost | 27% | 29% |

- Shippers are more likely to hesitate when the return is unclear.

- LSPs are more likely to struggle with integration.

Both issues point to the same broader challenge: companies need AI projects that connect cleanly to existing workflows and show measurable results early.

The Logistics Sector Clearly Wants AI-Enabled Operations

Companies that gain traction tend to start the same way: one repeated workflow, one visible bottleneck, one metric to track.

Practical starting points:

- Start with one workflow that creates repeated friction, such as order intake, quoting, route planning, shipment updates, or capacity forecasting.

- Choose use cases where the business cost is already visible. Manual corrections, planning delays, poor visibility, and inconsistent data are easier to justify than broad innovation goals.

- Define success before rollout. Track outcomes such as faster processing time, fewer intake errors, shorter planning cycles, or better forecast accuracy.

- Prioritize system fit early. In logistics, AI becomes more useful when it connects to TMS, ERP, order management, customer service, or tracking systems already used by the team.

- Move beyond use-case discovery quickly. Exploration has limited value unless someone owns the workflow, the metrics, and the implementation path.

- Use narrow wins to build internal support. A focused use case with measurable results usually creates a stronger foundation for expansion than a larger rollout with unclear value.

Finance Is Adopting AI Steadily, With Efficiency and Analytics Leading the Way

Financial services show strong AI uptake, but its center of gravity is still operational efficiency, analytics, and risk-sensitive workflows rather than broad transformation across every function.

NVIDIA's data suggests a sector that is advancing with purpose, especially in capital markets and consumer finance, while balancing performance gains against reliability, compliance, and skills concerns.

- 65% of financial services companies are actively using AI

- 42% are actively using or assessing agentic AI

- 89% say AI is helping both increase annual revenue and reduce annual costs

- 52% cite operational efficiency as one of the top ways AI improved the business in the last year

Adoption also varies by segment:

- 68% in capital markets

- 65% in consumer finance

- 62% in fintech

The main focus areas show that finance is still leaning on AI for analysis-heavy and process-heavy use cases:

The main focus areas show that finance is still leaning on AI for analysis-heavy and process-heavy use cases:

- 68% focus on data analytics

- 65% focus on generative AI

- 42% focus on agentic AI

- 42% focus on predictive analytics

- 35% focus on data processing

Top finance use cases include:

- 40% algorithmic trading

- 32% customer experience and engagement

- 30% document management

- 29% risk management

- 25% document processing and compliance

- 22% fraud detection

- 21% portfolio optimization

- 20% cybersecurity

AI agents in finance are being used most often where information handling and internal process control matter most:

- 56% knowledge management and retrieval

- 52% internal process optimization

- 43% customer support automation

- 38% task and project orchestration

- 35% regulatory compliance and risk monitoring

As adoption expands, governance gaps are becoming harder to ignore.

Cambridge Centre for Alternative Finance research found that 65% of organizations do not actively monitor AI systems for bias or fairness, while only 24% of regulators currently collect structured AI adoption data from financial institutions.

The biggest constraints are not hard to spot:

- 34% cite performance reliability issues

- 33% cite lack of internal skills or expertise

- 30% cite data-related issues

- 28% cite implementation issues

- 28% cite regulatory and ethical concerns

- 69% of financial institutions rely on OpenAI tools

Telecommunications Is Moving From Adoption to Measurable Performance Gains

Telecom shows strong year-over-year artificial intelligence growth in active use in NVIDIA’s report, unusually high confidence in AI’s productivity impact, and a direct link between AI deployment and both revenue and cost improvement.

Telecom shows strong year-over-year artificial intelligence growth in active use in NVIDIA’s report, unusually high confidence in AI’s productivity impact, and a direct link between AI deployment and both revenue and cost improvement.

- 66% of telecom companies are actively using AI, up from 49% in 2024 and 41% in 2023

- 29% are assessing or piloting AI

- 5% are not using AI

The financial and operational outcomes are especially strong:

- 90% say AI is helping increase annual revenue and reduce annual costs

- 67% say AI delivered more than a 5% increase in annual revenue

- 55% say AI delivered more than a 5% reduction in annual costs

- 99% say AI has improved employee productivity

That productivity impact breaks down further into different levels of gain:

- 10% report significant productivity gains

- 16% report major gains

- 47% report notable improvement

- 26% report minor improvement

Telecom’s ROI story is tied closely to infrastructure and operations:

- 65% say network automation is being driven by AI

- 59% say network automation is among the top AI use cases driving ROI

- 50% cite network automation as a top AI ROI use case

- 41% cite customer service and experience optimization

- 33% cite internal process optimization

Generative and agentic AI are also becoming more mainstream in telecom:

- 60% are using generative AI

- 48% are using or assessing agentic AI

- 23% have already deployed AI agents

- 41% say network automation is the top use case for agentic AI

Even in a strong-performing sector, the barriers remain familiar:

- 54% cite data-related issues

- 47% cite lack of AI experts

- 34% say ROI is still unclear

Healthcare Adoption Is Rising, but the Value Story Varies by Segment

Healthcare shows broad AI adoption, but NVIDIA’s data makes it clear that this is not one unified market.

Healthcare shows broad AI adoption, but NVIDIA’s data makes it clear that this is not one unified market.

Pharma, biotech, providers, medtech, and digital health are moving at different speeds and focusing on different use cases.

The result is a sector with strong momentum, especially around data analytics and generative AI, but with clear differences in infrastructure, budget, and talent readiness.

- 70% of healthcare companies have adopted AI, up from 63% in 2025

- 69% are using generative AI and large language models, up from 54%

- 47% are actively using AI agents or assessing agent use cases

Healthcare’s most common use cases show a blend of operational and clinical priorities:

- 65% use AI for data analytics and data science

- 42% use AI to support clinical decision-making

- 42% use it for clinical decision support

- 38% use it for medical imaging

- 38% use it for administrative tasks

ROI also differs sharply by segment:

- 57% of medtech respondents report ROI from AI for medical imaging

- 46% of pharmaceutical organizations report ROI from AI for drug discovery and development

By segment, AI priorities look quite different:

| AI Priorities | Pharma and Biotech | Payers and Providers | Medtech, Tools, and Diagnostics | Digital Healthcare |

| Gen AI and LLMs | 74% | 72% | 55% | 77% |

| Data Analytics | 80% | 59% | 55% | 69% |

| Predictive Analytics | 61% | 46% | 45% | 55% |

| Agentic AI | 53% | 49% | 30% | 60% |

The sector’s barriers also reveal a scale problem between small and large organizations:

- 40% of small businesses cite lack of budget as a top challenge, versus 20% of large companies

- 33% of small companies cite insufficient data size for model training, versus 21% of large organizations

- 33% of large organizations cite lack of AI experts

- 39% cite data-related issues overall

- 37% cite regulatory and ethical concerns

AI Maturity by Stage: From Experimentation to Embedded Use

88% of Organizations Use AI, but Only a Minority Have Rebuilt the Business Around It

AI is now widely used across organizations, and generative AI has spread quickly into everyday business functions, but deep operational maturity remains much rarer.

Most companies are still in the stage of layering AI onto existing work rather than redesigning products, processes, or decision-making around it.

- Broad AI use is now common, but scale still has limits

- Most companies are still in the early or middle stages of maturity

- Autonomy remains tightly constrained in most companies

- The maturity gap explains why AI results remain uneven

Broad AI Use Is Now Common, but Scale Still Has Limits

Stanford’s 2026 AI Index shows that AI use is now mainstream at the organizational level.

- 88% of surveyed organizations now use AI

- 70% use generative AI in at least one business function

- AI agent deployment remains in the single digits across nearly all business functions

Many companies can say they are using AI, but far fewer can say AI is operating at scale across the business in a way that changes how work actually gets done.

Most Companies Are Still in the Early or Middle Stages of Maturity

Deloitte’s 2026 report gives one of the most useful maturity splits because it separates surface-level use from real process redesign and deeper business transformation.

Deloitte’s 2026 report gives one of the most useful maturity splits because it separates surface-level use from real process redesign and deeper business transformation.

The distribution shows that organizations are spread across three distinct stages, with the largest share still using AI in a limited way:

- 37% use AI at a surface level, with little or no process change

- 30% are redesigning key processes around AI

- 34% are starting to use AI to deeply transform products, services, core processes, or business models

- Surface-level use may improve efficiency at the margins, but it does not necessarily produce the same gains as process redesign or business-model transformation.

Autonomy Remains Tightly Constrained in Most Companies

Grant Thornton’s 2026 data supports the same maturity gap from the agentic AI side. Most organizations are still cautious about letting AI operate with real autonomy, especially in higher-risk settings.

- 5% allow agents to execute high-stakes decisions without human review

- 60% limit agents to moderate-risk task automation

- Nearly three in four organizations are giving agentic AI access to their data and processes

- 20% have a tested AI incident response plan

A company may be piloting or scaling agents, but if autonomy is tightly restricted and governance is weak, that organization is still operating in an early stage of trust and control.

The 2026 data suggests that many businesses are moving toward agentic AI, but most are doing so carefully and within narrow limits.

The Maturity Gap Explains Why AI Results Remain Uneven

Taken together, these AI statistics point to the same conclusion: AI adoption has become broad, but deep maturity is still limited.

The result is a market where AI presence is common, but AI-led transformation is still concentrated among a smaller group of organizations.

Lindsay Jessup, CEO of Geeks, adds that many AI statistics still overemphasize adoption while overlooking implementation success.

In her view, adoption without real organizational evolution can create new bottlenecks instead of measurable progress.

She argues that stronger outcomes come when AI moves beyond isolated experiments and becomes embedded in the way the business operates across its lifecycle.

A useful way to apply this data is to group AI initiatives by maturity rather than by tool type.

Separate experiments, embedded workflow use cases, and business-transforming deployments into different buckets.

That gives a much clearer picture of where your business actually stands and prevents surface-level adoption from being mistaken for strategic progress.

AI Statistics by Business Function: Where Companies Are Using It Most

Marketing and Sales Leads on Revenue Impact, While Software Engineering and IT Deliver the Strongest Cost Savings

Some functions are using AI most heavily because the work is information-dense and repetitive, while others are producing stronger revenue or cost results because AI is improving decision-making, output speed, and workflow efficiency in measurable ways.

- The most common AI use cases are clustered in a few high-fit functions

- Marketing, strategy, and product functions are most tied to revenue gains

- Software engineering, manufacturing, and IT are where cost savings show up most clearly

The Most Common AI Use Cases Are Clustered in a Few High-Fit Functions

Stanford’s 2026 AI Index shows that the strongest AI-use pairings tend to appear where the technology has a clear operational fit.

Stanford’s 2026 AI Index shows that the strongest AI-use pairings tend to appear where the technology has a clear operational fit.

These are functions where AI can support knowledge-heavy work, accelerate production, or improve decisions without requiring a full business-model overhaul.

- 58% knowledge management in business, legal, and professional services

- 58% software engineering in technology

- 56% IT in technology

- 51% marketing and sales in consumer goods and retail

- 43% risk, legal, and compliance in financial services

Knowledge management, engineering, IT, and compliance are all functions where speed, retrieval, consistency, and automation can create visible gains quickly.

Marketing, Strategy, and Product Functions Are Most Tied to Revenue Gains

Stanford’s 2026 data separates where AI is being used from where it is creating financial impact.

Stanford’s 2026 data separates where AI is being used from where it is creating financial impact.

On the revenue side, the strongest associations appear in functions tied to growth, planning, and offer creation:

- 67% marketing and sales

- 65% strategy and corporate finance

- 62% product and service development

- 59% supply chain management

AI seems to drive revenue most clearly when it improves how companies attract demand, make strategic decisions, develop offerings, or manage the flow of goods and services.

These are functions where better forecasting, faster iteration, stronger targeting, or more responsive operations can translate into measurable business growth.

Software Engineering, Manufacturing, and IT Are Where Cost Savings Show Up Most Clearly

The functions most associated with cost reduction are the ones where work is structured, repeatable, and easier to optimize directly.

The functions most associated with cost reduction are the ones where work is structured, repeatable, and easier to optimize directly.

That makes them especially important for companies trying to prove early AI value through efficiency rather than top-line growth:

- 56% software engineering

- 56% manufacturing

- 54% IT

- 53% strategy and corporate finance

Cost savings tend to show up first where workflows are well defined and performance can be tracked cleanly.

- Software engineering and IT benefit from faster output, code assistance, and workflow automation.

- Manufacturing benefits from process optimization and quality control.

- Strategy and corporate finance appears in both revenue gains and cost savings, which suggests it may be one of the few functions where AI can support both better growth decisions and leaner execution.

AI by Use Case: What Companies Actually Want It To Do

Customer Support Is Emerging as AI’s Next Big Battleground, While Search, Knowledge, and Content Still Lead GenAI Use Cases

AI impact is shifting from broad experimentation to a smaller set of functions where leaders expect the next wave of value to land.

For generative AI, the strongest expected impact is clustered around search, knowledge access, virtual assistants, chatbots, and content generation.

For agentic AI, the center of gravity is moving toward customer support, with supply chain, R&D, knowledge management, and cybersecurity also standing out as high-potential use cases.

- Search, chatbots, and content remain the strongest GenAI use cases

- Customer support is becoming one of the clearest near-term agentic AI use cases

- Real-world AI use is diversifying beyond the earliest breakout tasks

Search, Chatbots, and Content Remain the Strongest GenAI Use Cases

Deloitte’s 2026 State of AI shows that the most defensible use-case framing are the categories leaders expect to reshape their industries most.

On the GenAI side, the leading use cases are all tied to how organizations find, generate, and deliver information faster.

- Search and knowledge management

- Virtual assistants and chatbots

- Content generation

These use cases sit close to everyday work, scale across teams, and solve visible business problems such as information retrieval, self-service, faster communication, and content production.

Customer Support Is Becoming One of the Clearest Near-Term Agentic AI Use Cases

Deloitte’s 2026 data says agentic AI is expected to have its highest impact in customer support, with supply chain management, R&D, knowledge management, and cybersecurity also seen as strong candidates for the next wave of impact.

Thiago Maior, CEO of EZOps Cloud, says AI is changing customer service by making responses faster and more natural through smart chatbots and assistants.

He adds that results depend not just on the tools themselves, but on training teams properly and building trust through strong data security practices.

That lines up well with Gartner’s 2026 customer-service data, which gives the cleanest numeric proof that service is one of the hottest near-term AI use cases.

- 91% of customer service leaders say they are under pressure to implement AI in 2026

- Nearly 80% expect to transition at least some agents into new roles

- 84% plan to add new skills to the agent role

- 58% aim to upskill agents into knowledge management specialists

AI in service is increasingly tied to customer satisfaction, self-service success, and the redesign of frontline work.

Real-World AI Use Is Diversifying Beyond the Earliest Breakout Tasks

Anthropic’s March 2026 Economic Index shows how AI use is actually spreading in practice.

On Claude.ai, 35% of conversations were tied to computer and mathematical tasks, which kept coding as the most common use.

At the same time, the top 10 tasks fell from 24% to 19% of conversations, showing that usage is diversifying beyond the narrow set of early tasks that dominated initial adoption.

- Coding remained the most common use

- Business sales and outreach automation was among the API workflows whose share at least doubled

- Automated trading and market ops was also among the API workflows whose share at least doubled

This shows that technical use cases still dominate a large share of usage, but the mix is broadening as AI moves into more business-facing and workflow-driven applications.

AI Statistics by Company Size: Who Is Moving Faster

Large Enterprises Are Pulling Ahead in AI, With Adoption Reaching 55% Versus Just 17% for Small Firms

Large enterprises are adopting AI at much higher rates, using a wider mix of technologies, and investing at levels that most smaller firms are nowhere near matching.

That makes company size one of the strongest ways to show that AI progress is not evenly distributed across the market.

In The EU, The Adoption Gap Gets Wider As You Move From Use to Breadth of Use

Eurostat’s 2026 report shows a sharp size-based divide in AI adoption across European enterprises.

Eurostat’s 2026 report shows a sharp size-based divide in AI adoption across European enterprises.

In 2025, large enterprises were far more likely than medium or small businesses to use AI technologies at all, and the gap widened further when measured by how many AI technologies they were using at once.

- 55.0% of large enterprises used AI technologies

- 30.4% of medium enterprises used AI technologies

- 17.0% of small enterprises used AI technologies

The same pattern becomes even clearer when looking at breadth of use rather than basic adoption:

- 44.0% of large enterprises used at least two AI technologies

- 20.8% of medium enterprises used at least two AI technologies

- 10.6% of small enterprises used at least two AI technologies

The data shows that the size gap is not only about whether companies use AI, but also how deeply AI is spreading into their operations. Large firms are more likely to move beyond a single tool or pilot and into broader, more layered adoption.

In The United States, AI Adoption Is Still Concentrated in Larger Employers

The Federal Reserve’s 2026 note gives one of the strongest US signals that AI adoption is concentrated among bigger firms:

- 18% of US firms had adopted AI by the end of 2025

- 78% of the labor force worked at firms that had adopted AI

Firm-level adoption is still limited, but worker exposure is already much broader because adoption is concentrated in companies with larger workforces.

AI Workforce and Employment Statistics

170 Million New Jobs Could Be Created by 2030, but 59% of Workers Will Still Need Retraining

The labor market is heading toward large-scale role redesign, skills disruption, and uneven hiring shifts rather than one simple wave of job loss.

- AI is set to change the workforce more through transition than through pure replacement

- Skills are becoming the main workforce bottleneck

- Workers are adopting AI faster than many firms are redesigning work around it

- AI is already affecting pay, productivity, and worker value

AI Is Set To Change the Workforce More Through Transition Than Through Pure Replacement

The World Economic Forum’s Future of Jobs Report 2025 shows us how workers move into new roles, and whether employers can build the skills pipeline to support that shift.

The World Economic Forum’s Future of Jobs Report 2025 shows us how workers move into new roles, and whether employers can build the skills pipeline to support that shift.

- 22% of jobs are expected to be disrupted by 2030

- 170 million new roles could be created

- 92 million roles could be displaced

- 78 million net new jobs could result

That does not make the transition easy. The same WEF data shows the pressure will fall heavily on skills and redeployment rather than on headcount alone.

Skills Are Becoming the Main Workforce Bottleneck

The workforce story in 2025 and 2026 is increasingly about whether workers can keep up with changing job requirements. WEF reports that:

- 39% of workers’ core skills are expected to change by 2030

- 59% of the global workforce will need reskilling

- 63% of employers cite skills gaps as their top transformation barrier

- 85% of employers plan to prioritize workforce upskilling

- Two-thirds plan to hire talent with specific AI skills

- 40% anticipate reducing workforce where AI can automate tasks

- 50% plan to reorient their business in response to AI

Even if net jobs rise, workers still face a large-scale skills reset, and employers are already planning around it.

Workers Are Adopting AI Faster Than Many Firms Are Redesigning Work Around It

PwC’s 2025 Global Workforce Hopes and Fears Survey found that:

- 54% of workers used AI in their jobs in the past year

- About three-quarters of users say AI improves productivity and work quality

- 14% use GenAI daily

- 6% use agentic AI daily

Gallup’s April 2026 data shows a similar pattern in the US workforce:

- 50% of US employees use AI at work at least a few times a year

- 13% use AI daily

- 28% use AI a few times a week or more

- 41% say their organization has integrated AI tools

AI is already present across large parts of the labor market, but routine use is still much narrower than topline adoption numbers suggest.

AI Is Already Affecting Pay, Productivity, and Worker Value

The 2025 PwC AI Jobs Barometer found that workers with AI skills earned:

- 56% average wage premium for workers with AI skills

- 3x higher growth in revenue per employee in AI-exposed industries

- 38% growth in job availability for more AI-exposed roles

- 66% faster change in employer skill demand in AI-exposed jobs

The data also shows that workers who can use AI well are becoming more productive and, in many cases, more valuable.

AI Consumer Statistics: How People Actually Use AI Day to Day

61% of US Adults Have Used AI in the Past Six Months, Showing That Consumer AI Is Moving From Experiment to Habit

AI adoption is growing quickly, but trust, data concerns, and differences in how often people use AI still shape what consumer AI really looks like in practice.

AI adoption is growing quickly, but trust, data concerns, and differences in how often people use AI still shape what consumer AI really looks like in practice.

- Consumer AI use is becoming mainstream, but daily reliance is still narrower

- Service and routine assistance are becoming part of everyday AI behavior

- AI is becoming part of how people access information and news, especially younger users

Consumer AI Use Is Becoming Mainstream, but Daily Reliance Is Still Narrower

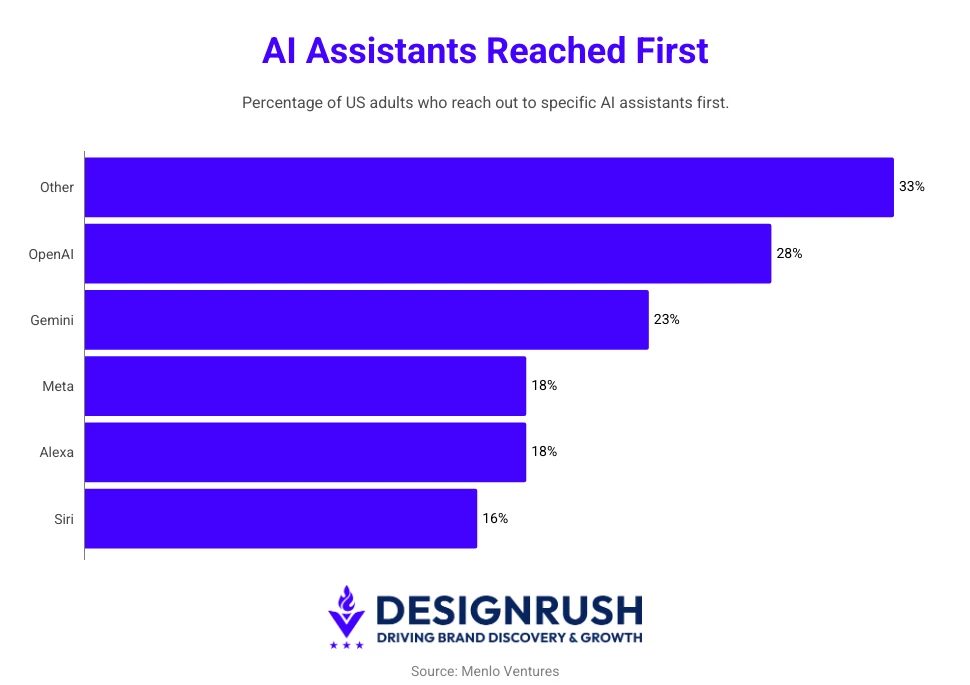

Menlo Ventures’ 2025 consumer AI survey found that:

- 61% of US adults used AI in the past six months

- Nearly one in five rely on it every day

That said, broad exposure does not mean everyone is using AI constantly.

The consumer story is stronger when you separate tried it, use it regularly, and depend on it day to day.

Those are very different levels of engagement, and the 2025 to 2026 data shows that the market is still spread across all three.

Service and Routine Assistance Are Becoming Part of Everyday AI Behavior

Capgemini’s 2026 consumer research shows that AI is also moving into recurring service and assistant-like roles:

- 52% use virtual assistants for automated tasks at least once a week

- 76% want clear rules for when an assistant is allowed to act

The strongest consumer use cases are often not dramatic, but routine, repeatable, and practical: reordering, planning, assistance, follow-up, and quick problem-solving.

AI Is Becoming Part of How People Access Information and News, Especially Younger Users

Reuters Institute’s 2025 and 2026 research adds an especially valuable consumer behavior signal:

- 7% use AI for news weekly overall

- 15% of under-25s use AI for news weekly

- Weekly AI use for getting information rose from 11% to 24%

- AI use for creating media reached 21%

These numbers are still relatively small compared with overall internet behavior, but they are important because they show where daily AI use is gaining ground fastest: information discovery, news access, and lightweight assistance.

AI Trust and User Sentiment Statistics: Everyday Use Is Growing, but Skepticism Remains

50% of Americans Feel More Concerned Than Excited About AI, Even as Everyday Use Keeps Growing

People are increasingly using AI for work, search, assistance, and everyday tasks, but trust remains fragile.

- Public sentiment is still more cautious than enthusiastic

- Usage is rising, but sentiment is not automatically improving with it

- Data use and control are major trust barriers for consumers

Public Sentiment Is Still More Cautious Than Enthusiastic

Pew’s March 2026 findings offer one of the clearest snapshots of broad AI sentiment in the US:

Pew’s March 2026 findings offer one of the clearest snapshots of broad AI sentiment in the US:

- 50% of Americans say the growing use of AI in daily life makes them feel more concerned than excited

- 10% say they feel more excited than concerned

- 38% say they feel equally concerned and excited

People may find AI useful, but many still do not feel fully at ease with its broader role in society.

Usage Is Rising, but Sentiment Is Not Automatically Improving With It

Quinnipiac’s March 2026 poll reinforces the same pattern from a different angle. It found that Americans’ use of AI is increasing, but their views are becoming more negative, especially around daily-life impact and jobs.

- 55% say AI will do more harm than good in daily life

- 70% think AI advances will reduce job opportunities

- 74% say the government is not doing enough to regulate AI

- 30% worry AI could make their own job obsolete

Data Use and Control Are Major Trust Barriers for Consumers

Capgemini’s 2026 consumer data shows that trust weakens quickly when people feel they are losing visibility or control over how AI works.

Consumers are interested in AI-powered assistance, but they want clear boundaries around what these systems can do and how their data is handled.

- 71% of consumers are concerned about how generative AI uses their information

- 76% want the ability to set clear rules for when an AI assistant is allowed to act

What Is Still Slowing AI Adoption Down

Lack of AI Expertise Is the Top Barrier Across Company Sizes, While Governance Confidence Remains Strikingly Low

Across regions and surveys, the biggest blockers are skills, data governance, legal uncertainty, and the lack of confidence needed to scale AI safely into real workflows.

- Skills remain the most common reason companies stop short of adoption

- Privacy and legal uncertainty are still major adoption blockers

- Workforce readiness is now one of the biggest scaling challenges

- Governance confidence is much weaker than AI ambition

Skills Remain the Most Common Reason Companies Stop Short of Adoption

Eurostat’s 2026 report shows that among enterprises that considered AI but did not adopt it, the leading barrier was a lack of relevant expertise:

Eurostat’s 2026 report shows that among enterprises that considered AI but did not adopt it, the leading barrier was a lack of relevant expertise:

- 70.9% of small enterprises cite lack of relevant expertise

- 69.2% of medium enterprises cite lack of relevant expertise

- 65.1% of large enterprises cite lack of relevant expertise

Smaller companies feel it most sharply, but even large enterprises report expertise gaps at very high levels.

Privacy and Legal Uncertainty Are Still Major Adoption Blockers

Eurostat’s 2026 data also shows that non-adopters are still heavily constrained by governance-related concerns, especially around privacy and legal exposure:

Eurostat’s 2026 data also shows that non-adopters are still heavily constrained by governance-related concerns, especially around privacy and legal exposure:

- 52.5% of small enterprises cite data protection and privacy concerns

- 52.3% of medium enterprises cite data protection and privacy concerns

- 58.8% of large enterprises cite data protection and privacy concerns

- 54.8% of small enterprises cite legal uncertainty

- 49.4% of medium enterprises cite legal uncertainty

- 51.2% of large enterprises cite legal uncertainty

Even when organizations want AI, many still do not feel fully prepared to handle the compliance, privacy, and legal implications that come with wider deployment.

Workforce Readiness Is Now One of the Biggest Scaling Challenges

Deloitte’s 2026 State of AI identifies insufficient worker skills as the biggest barrier to integrating AI into existing workflows, which helps explain why many organizations can launch tools faster than they can embed them productively into day-to-day work.

The most common responses Deloitte found are all talent-focused:

- 53% are raising overall AI fluency

- 48% are upskilling and reskilling workers

- 36% are hiring specialized talent

“The biggest challenges in implementing AI are data quality, system integration, and closing the skills gap,” explains Alex Benedychuk, CEO of Regis Team.

He says companies move forward more effectively when they improve data practices, build cross-functional teams, and adopt AI in phases rather than trying to force broad rollout too early.

Governance Confidence Is Much Weaker Than AI Ambition

Grant Thornton’s 2026 AI Impact Survey shows that a large majority of executives say they do not have strong confidence that their organizations could pass an independent AI governance audit on short notice, which is one of the clearest signs that deployment is moving faster than control frameworks.

- 78% of executives lack strong confidence they could pass an independent AI governance audit within 90 days

- 5% allow agents to execute high-stakes decisions without human review

- 60% limit agents to moderate-risk task automation

Many companies may be piloting or deploying agents, but very few are comfortable letting them operate independently in high-stakes settings.

AI Budget Trends and Where Companies Plan To Invest Next

Worldwide AI Spending Is Set to Reach $2.52 Trillion in 2026, Showing That Companies Are Funding AI at Scale

Global outlays are rising sharply, most firms expect to invest this year, and the biggest spending is flowing into infrastructure, services, and the foundations needed to make AI work in production.

Read on to find out budget and artificial intelligence trends for 2026.

- Global AI spending is rising fast, and infrastructure is taking the biggest share

- The investment gap is just as clear as the adoption gap

- The quality of AI spending matters as much as the amount

Global AI Spending Is Rising Fast, and Infrastructure Is Taking the Biggest Share

Gartner forecasts $2.52 trillion in worldwide AI spending for 2026, up 44% year over year from $1.76 trillion in 2025.

The largest category is AI infrastructure, followed by AI services, and AI software.

- $1.37 trillion for AI infrastructure

- $588.6 billion for AI services

- $452.5 billion for AI software

- $401 billion added by AI infrastructure alone in 2026

The largest share is not going only into end-user tools or model access. It is going into the technical base required to run AI widely, which is a much stronger sign of long-term commitment.

The Investment Gap Is Just As Clear as the Adoption Gap

The Atlanta Fed’s 2026 executive data shows that company size also shapes how much firms are willing or able to spend on AI.

- Nearly 60% of responding firms invested in AI in 2025

- 80% of large firms invested in AI in 2025

- Around half of small firms invested in AI in 2025

- More than 80% of firms expect to invest in AI in 2026

The same study says the main motivations are productivity and efficiency, not cost reduction, which is an important correction to the idea that companies are funding AI mainly to cut labor or operating expense.

The Atlanta Fed also found that firms see the biggest realized and expected benefits in improving production efficiency, enhancing decision-making speed, and improving output.

The difference becomes much sharper when measured by spending level:

- Around 30% of large firms expect to invest more than $1 million in AI in 2026

- 1% of smaller firms expect to invest more than $1 million

- Nearly 60% of smaller firms plan to invest less than $20,000

- 14% of larger firms plan to invest less than $20,000

Many firms may say they are investing in AI, but the scale of that investment is nowhere near comparable.

A company testing a few tools with a five-figure budget is in a very different position from one funding seven-figure deployment, integration, and process change.

The Quality of AI Spending Matters As Much as the Amount

Gartner’s April 2026 foundation study adds the most important quality-of-spend takeaway in this section.

Organizations with successful AI initiatives invest up to four times more as a share of revenue in foundational areas such as data quality, governance, AI-ready talent, and change management than organizations reporting poor AI outcomes.

- Successful AI organizations invest up to 4x more in foundations as a share of revenue

- Key spending areas include data quality, governance, AI-ready people, and change management

Two companies may both say they are investing in AI, but the one funding data readiness, governance, talent, and organizational change is much more likely to turn that spend into durable business results.

- Gartner also found that only 39% of technology leaders are confident their current AI investments will have a positive impact on financial performance.

That gap shows that companies are clearly committing budget, but many are still unsure whether that spending will translate into measurable return.

Our team ranks agencies worldwide to help you find a qualified partner. Visit our Agency Directory for the top AI companies, as well as:

- Top AI App Development Companies

- Top AI Product Development Companies

- Top AI Web Design Companies

- Top AI Marketing Companies

- Top AI Market Research Companies

AI Statistics FAQs

1. Which business areas are using AI the most?

AI tends to appear most often in functions where work is knowledge-heavy, process-driven, or easy to measure, such as marketing, sales, software development, IT, customer service, and operations.

2. Which AI use cases are growing fastest?

Search, knowledge management, virtual assistants, chatbots, content generation, customer support, and workflow automation continue to stand out as leading use cases because they solve visible business problems and can scale across teams.

3. Are companies getting real business value from AI?

Yes, but the value is uneven. Many companies report gains in productivity, efficiency, and decision-making first, while fewer have turned AI into clear revenue growth or broader business transformation.

4. Why do some companies get more value from AI than others?

The strongest results usually come from companies that move beyond pilots, integrate AI into real workflows, and support adoption with data readiness, governance, talent, and process change. Companies with surface-level use tend to see narrower results.

5. What are the biggest barriers to AI adoption?

The most common blockers are limited internal expertise, workforce readiness gaps, privacy and legal concerns, weak governance, and difficulty embedding AI into existing systems and workflows.

6. What do AI budget trends reveal?

AI budget trends show whether companies are treating AI as a long-term capability or a short-term experiment. They also reveal which organizations are funding the infrastructure, talent, and governance needed to support AI in production.

7. How should companies use AI statistics in practice?

They should use them to benchmark their own adoption stage, compare their priorities with the broader market, identify realistic starting points, and focus investment on workflows where business impact can be measured clearly.